Google's artificial intelligence unit, DeepMind, is using blockchain technology to build an auditing system for analyzing and storing healthcare data; the system will mainly focus on tracking all of a person's hospital health data and centrally storing it for access and ownership by individuals; DeepMind will also make its system available through open source software allowing for the technology to be utilized for broader solutions including auditing identities, financial records and private corporate data. Source

digital transformationEmbedded Financeenterprise blockchainexchanges / cap mktsmega banksneobankOpen Bankingopen source

·In this analysis, we focus on Goldman Sachs launching an institutional embedded finance offering within Amazon Web Services, and Thought Machine raising a unicorn round for its cloud core banking platform. We explore these developments by focusing on the emerging role of cloud providers as distributors of third party software, think through some of the implications on standalone fintechs and open banking, and check in on AI company Kensho. Last, we highlight the difference between Web3 and Web3 approaches to “cloud”, and suggest a path as to how those can be rationalized in the future.

Recent research suggests that payday lenders are marketing directly to consumers who are seeking financial help due to the pandemic;...

A case study at the Harvard Business School was presented as part of the executive MBA program on the bank’s digital strategy; Goldman CFO Marty Chavez recently stated “Goldman is for risk what Google is for search”; the move to becoming a tech company is not easy as other areas of the bank do not see the same benefits; Goldman is clearly on the front edge of innovation in banking today. Source.

Square upgrades Cash App into a payment processing powerhouse, completing the loop between the consumer and merchant side of the house. Goldman Sachs acquires GreenSky, adding a lending business at the point of intent. This analysis connects these symptoms into a framework explaining the increasing integration between commerce and finance, and the increasing role that demand generation plays. That in turn explains how the attention and creator economies interconnect with financial services.

The main driver of today's entry is the news -- which has largely percolated -- that ConsenSys acquired Quorum from J.P. Morgan, as well as received an investment from the bank in the company. There is a lot of jargon in the blockchain industry, and I want to try to pull this news apart to explain why it is interesting both to incumbent financial services players, as well as meaningful to the developing decentralized finance industry.

Ireland has become a hub of technological innovation as big tech, fintech and big financial services companies set up shop in country as an alternative to the UK; “Ireland has always been quite an innovative country; it has to be because it is such a small market, you can’t just lean on the Irish market to produce a decent fintech business.” says Sinead Fitzmaurice, co-founder of TransferMate, to the FT; talent from Google and Facebook have not only started their own companies but have also moved into finance giants like Deutsche Bank; low corporate tax rates combined with the tech talent has help the country become an emerging fintech market. Source.

Most significant banks have a mobile app with features that allow individuals to conduct close to their entire banking life on their phones; keeping up with the operating systems from Apple and Google is a challenge for the banks; banks are not as nimble as fintech startups and so there is a lot more detailed of a process to go through when making technology updates; banks have learned that 80% of users update operating systems within the first month of a new release, which puts pressure on the banks to act quickly; talking to American Banker about staying current, Alice Milligan, the chief customer and digital experience officer of Citi's global cards business, said, "This requires us to stay at the cutting edge of device and operating system developments in the industry."; prioritizing what features are most important is key, not everything can get done quickly and this forces banks to make difficult choices; as more people use technology in their financial lives, banks and fintech companies will need to make sure they try to stay ahead of the curve. Source

·

[Editor’s note: This is a guest post from Lisa Weinberger, Director of Digital Marketing at CircleBack Lending. CircleBack Lending is a Silver sponsor...

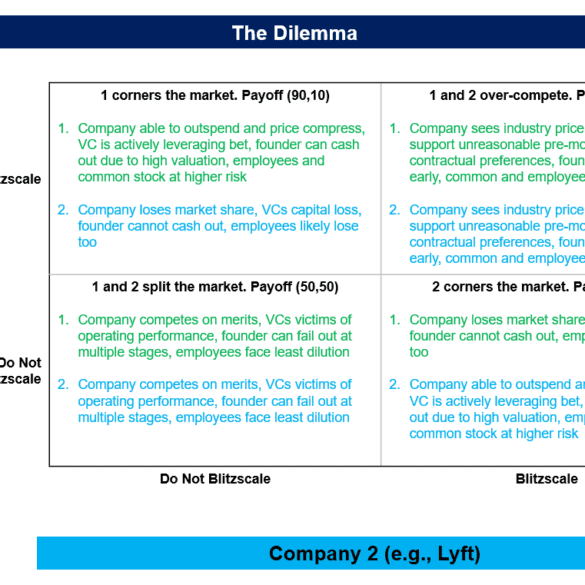

Why are high valuations bad? You've heard me talk about how the trend of Fintech bundling, and the unicorn and decacorn valuations led by SoftBank and DST Global, are creating underlying weakness in the private Fintech markets. Of course, they are also creating price compression and consolidation in the public markets (e.g, Schwab/TD, Fiserv/First Data) across sub-sectors. But public companies are at least transparent and deeply analyzed. Private companies have beautiful websites, charismatic leaders, and impressive sounding investors. Often when you look under the hood, it's just a bunch of angry bees trying to find something to sting.