This is a follow up to Stu Lustman’s two part series on Bitcoin P2P lending by Chris Grundy of Bitbond. Chris is an SEO Specialist, Bitcoin obsessive and avid tech fan who has written for a variety of Online publications as well as regularly contributing to the Bitbond blog. You can follow him on Twitter or connect with him on LinkedIn. Any feedback is welcome and encouraged.

Combining Forces -P2P lending and Bitcoin

P2P lending is having a stellar year. Indeed, the Peer-to-Peer Finance Association revealed that a record-breaking $792 million has been lent out through UK lending platforms in 2015 Q2.

Things in the U.S. look equally promising as Lending Club announced successfully breaking through $1.9 billion in originations in Q2. Prosper reported an equally impressive quarter, issuing $912.4 million in new loans, a 147% increase year-over-year.

With the P2P industry in such good health, why should you be interested in bitcoin based p2p lending?

Because bitcoin p2p lending allows you to do more with less as you will see in the following paragraphs. But first, how does bitcoin p2p lending work.

In short, bitcoin lending platforms can leverage the bitcoin payment network to create a global marketplace for loans. Importantly, most loans processed over these platforms are denominated in US dollars in order to mitigate bitcoin currency fluctuations.

This works by utilising an exchange rate pegged loan, which uses the US dollar as the underlying base currency. Payments are conducted in bitcoin only however, in order to reap the benefits of the bitcoin payment network. For a more comprehensive overview you can also read Bitcoin P2P lending – a primer in 8 steps. Now that we have a basic grasp of how it works, let’s have a look at the key advantages.

3 core advantages of bitcoin powered p2p lending

If you’re already seeing good results lending via established p2p lending platforms, here are reasons why you still might want to have a closer look at bitcoin powered p2p lending.

1. Diversify your portfolio globally

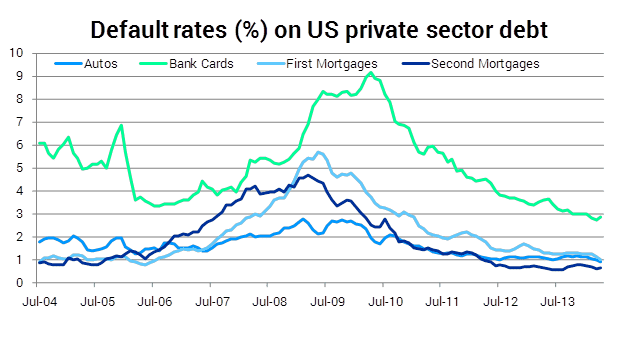

Credit risk is pro-cyclical. As shown by the graph below, in the event of a recession such as the one in 2009, defaults on private debt go up. When coupled with static nominal interest rates, this results in a decreased effective return on your loan portfolio.

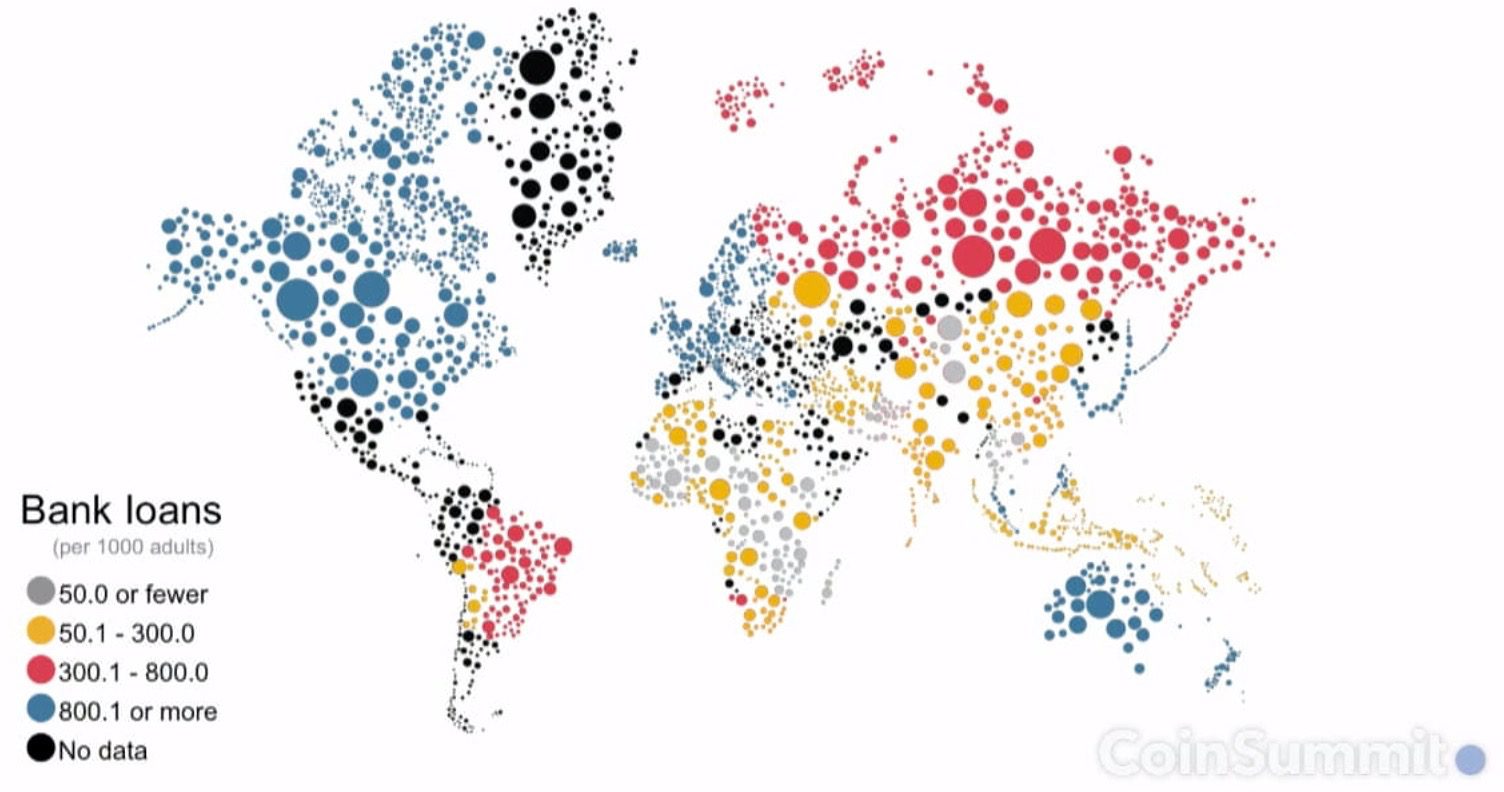

Investors on traditional p2p lending platforms are mostly exposed to one country only, meaning that they cannot diversify across different regions. With bitcoin based p2p lending, lenders have the ability to invest in different parts of the world, minimising risk from regional economic and political cycles.

Now, you might argue that events like the 2009 recession and subsequent financial crisis were global and international diversification would have made little difference to your ROI. However, we can assume that stronger growth rates correlate with better repayment rates on private sector debt. With this in mind it is important to note, that emerging markets still had an average growth rate of 2.3% in 2009, compared to the negative growth rates experienced by most developed economies.

Therefore a portfolio diversified across emerging and developed markets would likely have experienced a higher ROI, due to the resulting higher repayment rates. This means the investors who invest globally, may have been able to mitigate the effects of the recession that hit regional investors so hard.

2. Get access to higher interest rates

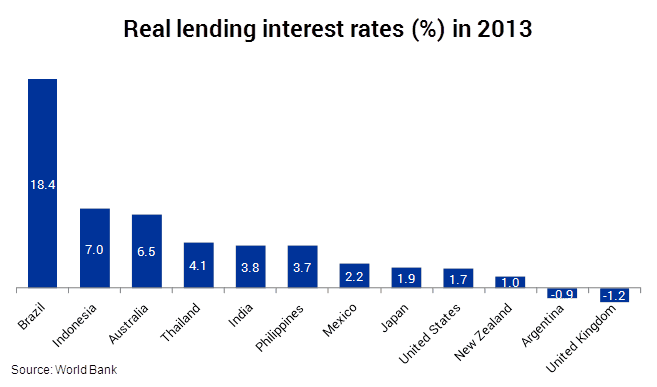

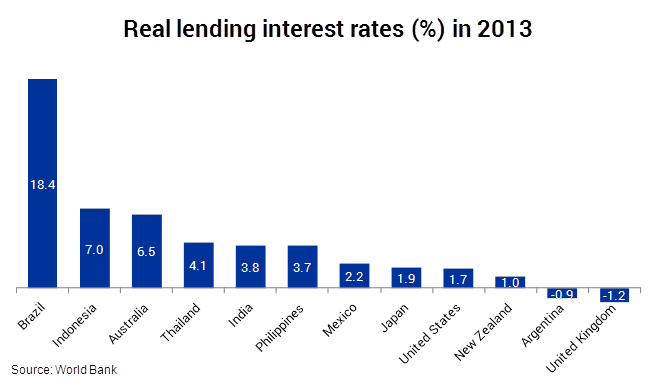

Bitcoin’s global reach allows investors access to higher interest rates. This is because borrowers from around the world command higher rates than U.S. and UK applicants.

As can be seen from the graph below, international borrowers are also accustomed to steep interest rates from banks, increasing the willingness to pay more than their U.S. and UK counterparts on cheaper p2p alternatives.

Looking at the risk/return ratio, it is important to understand that all loans on p2p bitcoin and traditional platforms have passed high quality standards to qualify for their application. The grade each loan listing receives should be viewed in this context.

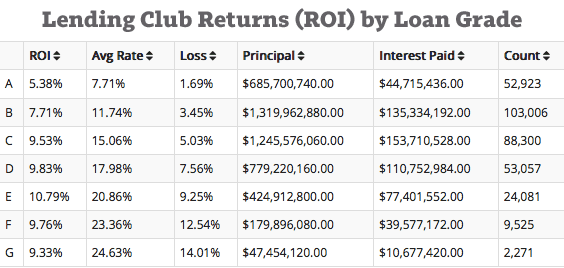

Finally, ROI should be the deciding factor for any investor to engage on a platform. Lending Club returns on grade “B” loans, by far the most popular, stand at 7.71%, with 10.79% as the largest average ROI (according to LendingMemo).

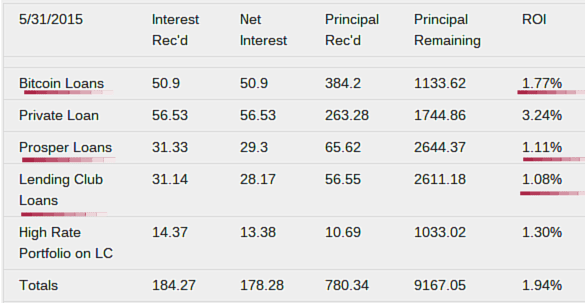

In contrast, ROI on bitcoin lending platforms aims to be higher. Bitbond’s expected ROI for example lies between 10% to 13%. Let’s take a look at Stu’s portfolio report for May to illustrate this point.

From the screenshot you can see bitcoin lending platforms can provide substantially higher monthly ROIs than their traditional counterparts. Consequently, early adopters like Stu and Marco from Smart Bitcoin Investment, are being joined by many others, as investors pour into the bitcoin lending space to take advantage of these high-yield opportunities.

3. Pay lower fees as an investor and borrower

Using bitcoin makes sense on a practical level as well. Due to the open-source nature of bitcoin as a technology and payment network, bitcoin based p2p lending platforms are independent from third parties like banks.

Bitcoin lending platforms like Bitbond offer lower fees than the traditional p2p lenders. These potential savings for investors and borrower are reflected in the table below.

| Loan originator | Borrower fees | Lender fees |

| LendingClub | 1.1-5% depending on credit grade | 1% on all amounts borrower pays |

| Prosper | 0.5-4.5% depending on credit grade | 1% annual servicing fee |

| FundingCircle | 2-5% depending on loan term | 1% annual servicing fee |

| Bitbond | 0.5-3% depending on loan term | 0% |

As can be seen, the p2p bitcoin lending platform, Bitbond, offers the smallest fees for borrowers, and lending is completely free.

Thus, we have established that p2p bitcoin lending is a viable alternative to its traditional counterpart with substantial benefits concerning risk, interest rates and fees. So what lending platforms should you know about and how do they differ?

Key players in the bitcoin lending field

Bitbond – the small business loans platform

The Berlin-based p2p bitcoin lending platform raised $675k in May 2015, bringing its total to just shy of $950k. The most recent funding has been used to improve usability and introduce new features for lenders.

Perhaps the most significant of these features for investors is the AutoInvest tool, which signals Bitbond’s commitment to rival the functionality of the established lending platforms. Launched at Finovate earlier this year, this tool provides investors with the opportunity to automate the lending process in order to maximise yields and reduce effort in asset allocation.

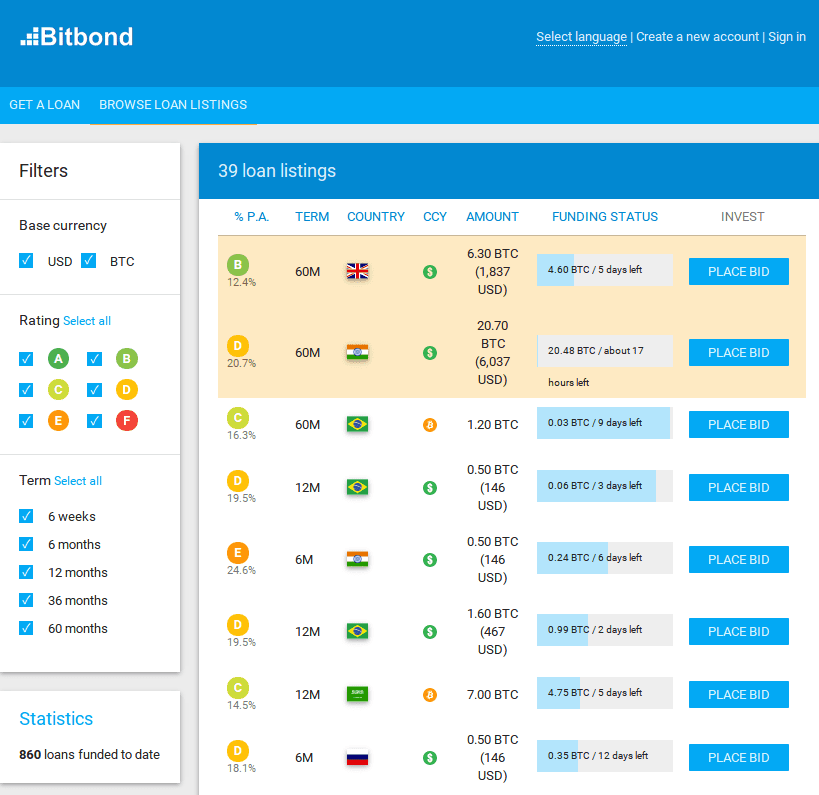

Usability has also been improved significantly. A screenshot of Bitbond’s loan listings page is below, showing all the available credit ratings, the country of residence, interest rates, the loan denomination as well as the terms and outstanding amount.

Furthermore, the German p2p bitcoin lending platform differentiates itself from its competitors by focusing on small business owners. By allowing borrowers to connect their eBay and PayPal accounts (among others), Bitbond gains an understanding of the creditworthiness of the applicant.

Specifically, an online seller with a carefully guarded reputation, large amounts of positive feedback and a good payments history on PayPal is unlikely to act fraudulently.

For investors, the average nominal interest rate at Bitbond is 18.5% p.a., which should be considered attractive.

Bitbond prides itself on transparency, meaning that it is the only one of the three bitcoin lending platforms which allows all relevant data to be downloaded in a csv file.

BTCJam – the leader in bitcoin personal and payday loans

The San Francisco based startup is the best capitalised of the three discussed here. Nevertheless, things have changed since Stu’s assessment in December, as growth has slowed and their competitors have gained ground.

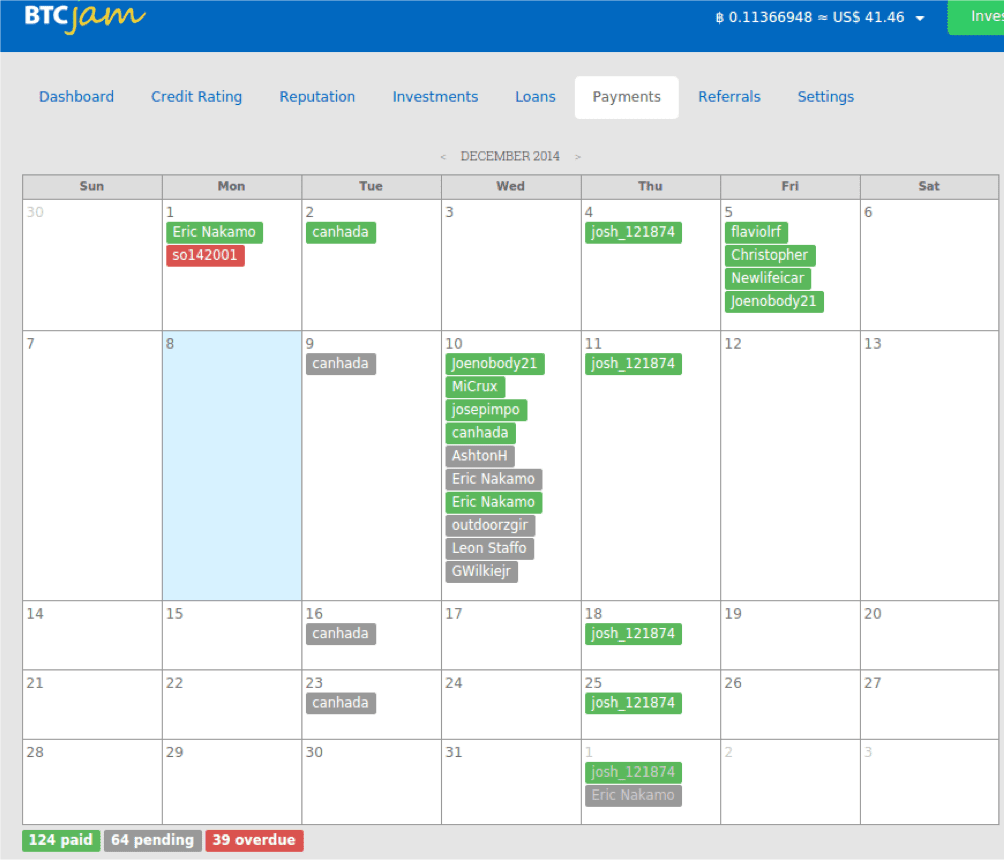

BTCJam still offers a great service however, providing a user friendly Receivables/Payables calendar page. Here, investors can get a good overview of upcoming repayments and plan their next investments accordingly.

Interestingly, BTCJam has recently tied borrower interest rates to credit scores and follows the example of Bitbond and traditional p2p lenders by applying risk-based loan pricing. The higher the credit score, the lower the interest rate. This represents another shift by a bitcoin lending company to provide similar functionality and UX to their traditional counterparts.

BTCJam has also played an important role in providing the legal precedent for a defaulted bitcoin loan. In a ruling earlier this year, a US judge ruled that a Kentucky man must repay an overdue loan he acquired via BTCJam. This verdict sets a crucial judicial instance, stating that overdue bitcoin loans are equal to overdue traditional loans in the eyes of the law.

Lastly, BTCJam offers the ability to trade notes on a secondary market, allowing investors to sell off portions of invested loans. Beneficially, this can be done on the site itself without having to revert to a separate market like FolioFN.

BitlendingClub – the follower in bitcoin personal and payday loans

The third and final key player in the bitcoin lending space is Illinois-based BitlendingClub. With $253k in funding, the startup has recently introduced some intriguing features, one of which is a loan voting system. On the platform, potential lenders are allowed to vote, raising the best loan applications to the front-page and attracting more lenders.

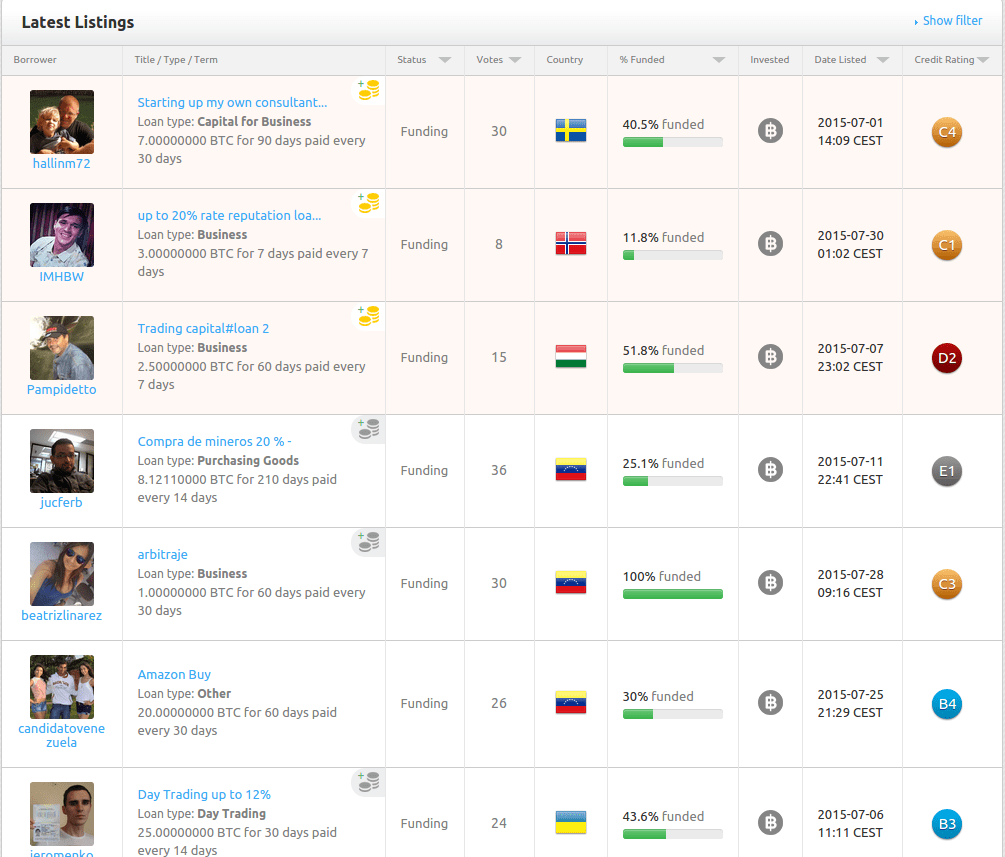

As can be seen from the screenshot, BitlendingClub employs a wider spectrum of credit rating than the other two, giving investors a more incremental overview of the potential risk involved.

Interestingly, the platform operates a dutch-auction style lending system, where borrowers submit a loan request and lenders can make loan offers. The borrower can accept the lowest offers which add up to the loan amount. All leftover offers are rejected automatically.

Another feature which sets BitlendingClub apart is the availability of key metrics on the homepage. These include the ROI, APR and default rates among others. BitlendingClub, like BTCJam, focuses on personal and payday loans, unlike Bitbond which specialises in loans for small business owners.

The future of bitcoin lending

Bitcoin lending has a promising future. Especially in regions like Latin America and Africa, which are underserved by the banking system and subsequently offer huge potential for digital currencies.

Mobile alternatives like MPesa (in Kenya) have already seen widespread adoption with over 17 million reported users. The day to day usage of digital or mobile currencies is significant because it lowers the entry barrier for bitcoin adoption in the world’s underserved regions.

For the 5 billion households with no bank account or access to traditional banking services such as loans, this could result in a financial revolution, as previously unbanked entrepreneurs and self-starters gain access to global working capital.

This represents a huge opportunity for investors who will gain access to so far unreachable regions and borrowers commanding attractive interest rates. The shift is recognised by the European Alternative Finance Report which sees online p2p lending as “the beginning of a broad and long-term structural change”.

These underserved regions are where the p2p bitcoin lending industry will see its fastest growth, as the potential for bitcoin adoption is tapped into by young African startups like TagPesa and Bitsoko. We are already seeing increasing demand from the world’s unbanked countries.

In the short term, bitcoin lending platforms will continue to benefit from enthusiastic early adopters, tech fans, entrepreneurs, shrewd investors and those neglected by the current financial system, as they in turn will benefit from bitcoin.

Bitcoin lending platforms offer an attractive alternative

Thus the bitcoin lending world has matured since Stu’s last appraisal, and is expanding its message globally. For the sake of balance however, it is important to realise that P2P bitcoin lending is still in its early stages with potential for improvement. One such area is doubtless the credit scoring of international borrowers which needs to be standardized and fed with more data.

What bitcoin technology enables is global, instant, cheap and frictionless transactions. Similarly to an email, users can send bitcoins to any location in the world and be sure of arrival in seconds, avoiding transfer and exchange fees. As we have seen this disruptive technology represents the next step in the evolution of p2p lending marketplaces as it enables cross-border lending and global diversification.

The first p2p lending platform Zopa started in 2005. Now with 10+ years in existence its viability is undoubted. Bitcoin p2p lending is only 2.5 years young. But the existing players are learning fast from their established counterparts and will likely reach a comparable level of sophistication faster.