Fresh off the back of the Terra-Luna collapse last year, BCG published a report that said despite a slowdown in trading volumes and crypto market cap, tokenization of illiquid assets was predicted to reach $16 trillion within the next decade.

An FTX meltdown, some bank failures supposedly tied to crypto, and multiple SEC enforcement actions later, the picture may not look so rosy.

However, Citi Group still seems to be raving about the sector. The group released a report in March 2023, stating that tokenizing financial and real-world assets was still a “killer use case.” for blockchain technology.

While the report acknowledged that the promise of blockchain had been talked about for a few years, tokenization could still be the function that tips it over the edge into mass usage. Citi predicted it could reach between $4-5 trillion by 2030. While this is a far cry from BCG’s $16 trillion, Citi noted that “momentum on adoption has positively shifted” (no doubt a great disappointment to the SEC).

The reason for this belief? Citi’s study has found that governments, large institutions, and corporations have continued developing blockchain-based tools. Now, they are said to have moved from investigating the benefits of tokenization to trials and proofs of concept.

“It just makes f*****g sense,” said Maex Ament, Co-Founder of Centrifuge. “It’s just there is no discussion anymore. To put assets on-chain – it’s just cheaper for everybody.”

“Only for the middlemen, where it doesn’t make sense for them, they push back. The rest of the world understands that it’s a superior technology.”

Could we still be on the brink of a tokenized revolution despite a slowdown?

RELATED: What crypto winter? Digital asset tokenization a $16-trillion business opportunity

The FTX effect

Ament explained that FTX’s collapse had caused a significant roadblock to adopting real-world asset tokenization.

“We are still only scratching the surface. Institutional money is still not coming in. We’re still experimenting,” he said. “The real money is just waiting on the sidelines. No one has done anything substantial in my book yet.”

“That was different nine months ago. We felt nine months ago it would happen. And then FTX happened…They put on the brakes in November, and we still haven’t recovered.”

Even Citi’s report, despite their multi-trillion-dollar prediction, felt adoption in the next few years was unlikely. Instead, they stated that mass adoption could still be “six to eight years away.”

“I do believe that the C-level suites, the boardrooms are still suffering from the FTX dilemma,” Ament continued. “It’s pretty astonishing how many people lost money in FTX. They just had their feet into something which they deemed secure. And then they got completely wiped out.”

“In a year from now, maybe again, the big institutional money will flow in. I think just time is needed.”

A revamp of the financial system’s back end

According to Citi, Ament, and many others researching tokenization, the technology just “makes sense.”

Blockchain, as a disruptive technology, is an outlier. However, the Citi report says that unlike other technologies (like Generative AI), its potential for disruption lies deep in the financial system – a highly regulated area with strong ties of fear and insecurity and a web of legacy systems.

As such, caution has surrounded the mass adoption, and despite the crypto drama, it lacks the “sex appeal” of general-use AI.

“To be sure, blockchain is not about to have a ChatGPT moment,” states the report. “Blockchain is a back-end infrastructure technology, more akin to cloud computing than artificial intelligence (AI) or the metaverse, which have a more prominent consumer interface.”

“Mass adoption for AI could be as early as two to four years driven by the recent rapid increase in data availability and computing power, improved algorithms, and models that have led to products such as ChatGPT, which have caught mass public attention.”

“Blockchain, on the other hand, could take longer for mass adoption (six to eight years perhaps) due to the need for collaboration among participants, standardization of platforms, and interoperability and compatibility with existing systems and software.”

However, if adopted, the benefits to the financial system are paralleled by a few other innovations.

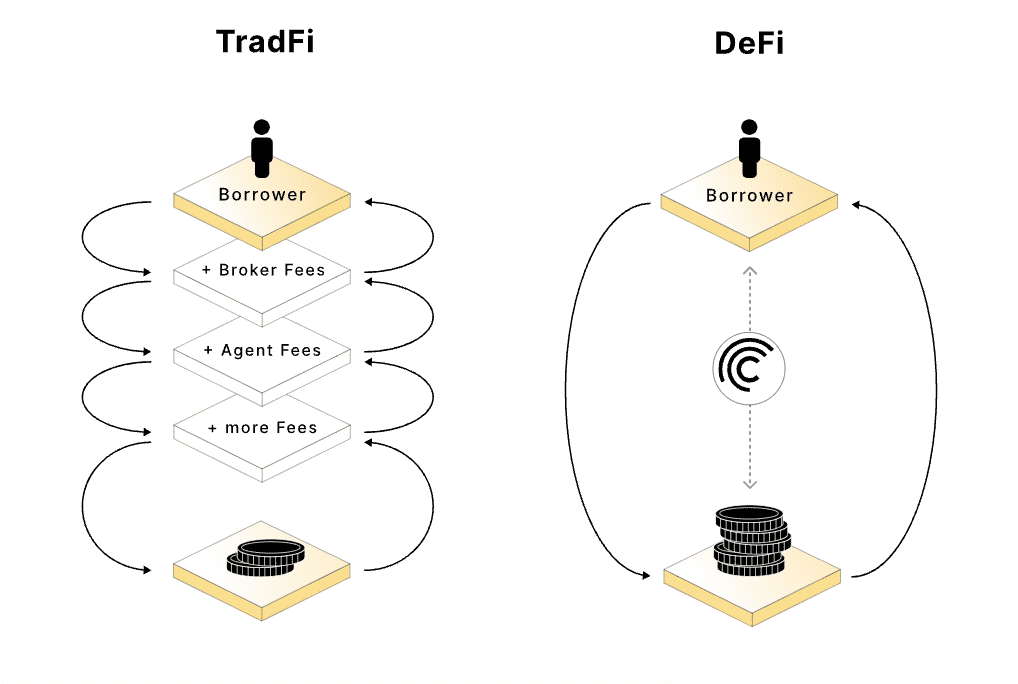

“At the end of the day, it boils down to price. Its transparency, speed, interoperability, and compostability also result in cheaper transactions and better price,” said Ament.

He explained that, in addition, on the level of currency tokenization, as seen with stablecoins, it could also fulfill the crypto promise of improving global access to wealth. The lack of national boundaries proposed by the blockchain allows access from all over the world to on-chain assets. This has already allowed for innovations such as cross-border lending protocols.

Launching Centrifuge Prime

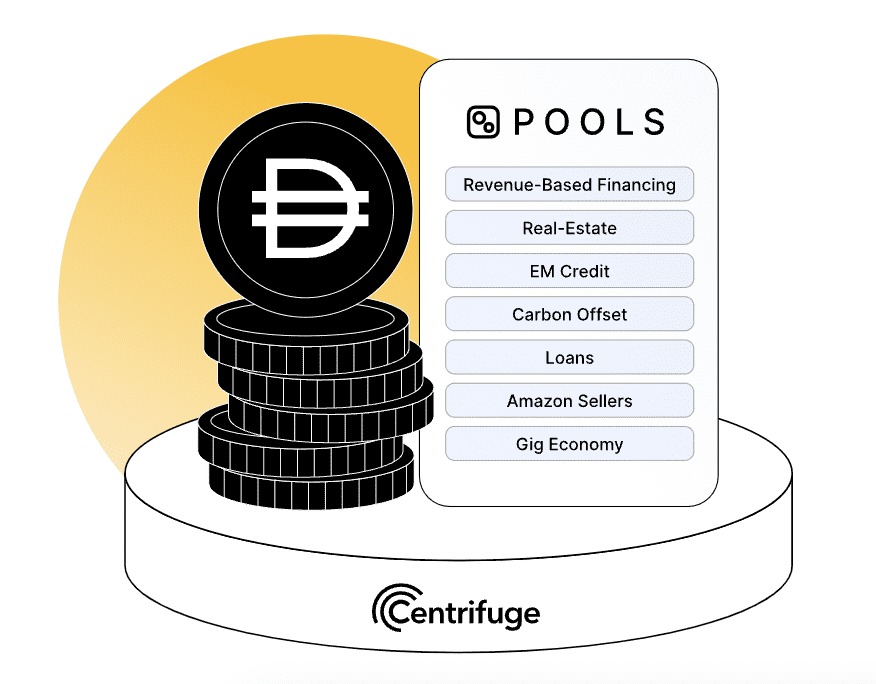

Centrifuge has made significant progress in lending and investment, working between on-chain and real-world assets. The company recently launched a suite of products directed at DAOs, allowing them to diversify into real-world assets and create new revenue streams.

Simultaneously, Centrifuge’s lending pools are financing sources for real-world businesses and asset owners.

“DAOs sit on stablecoins and get nothing for it,” explained Ament. “Right now, you sit on USDC. The only person that makes money with USDC is Jeremy of Circle. He makes four or 5% on Treasury. Why shouldn’t the DAO with 20 million sitting in stablecoins not get some return on it?”

“(With Centrifuge Prime), we make it incredibly easy for DAOs to take those assets and just put them in a Centrifuge pool. You get a 6-7% return on a very boring, safe asset, almost as safe as a stablecoin. And you get 6% without leaving the blockchain and investing through Centrifuge in something that has a real-world impact.”

Once in the lending pools, the assets go towards financing real-world assets, including asset-backed securities and real estate, which the company says offer a source of “predictable and sustainable yields.”