More than $445bn was lost to cyber crime last year, a 30 percent increase from three years earlier; banks have...

PeerIQ released their Q4 2018 Lending Earnings Insights Report which points to a number of themes showing the economy is strong...

New York City’s Metropolitan Transit Authority has partnered with Visa to launch a tap to pay system for subways and...

While announcing earnings for Q3 Wells Fargo and Bank of America both revealed how important digital channels are to their bottom line; BofA saw mobile banking users jump 11 percent, mobile usage grew at 19 percent and digital payments grew 9 percent in the past year; Wells Fargo saw digital usage grow 2 percent and digital sessions grow 6 percent; the digital trend shows how much banks businesses are changing. Source.

Wells Fargo was in the news for all the wrong reasons last week as a reported fire triggered an outage...

Wells Fargo customers are skeptical about the reason why they were unable to access accounts; the bank said there was...

Wells Fargo, Morgan Stanley, JPMorgan Chase and others have launched or will launch their own robo products to compete with slicker startups; after seeing the success of startups in the space the banks realized they needed to improve their offerings to keep customers and attract newer, younger ones; the trend to move away from white labeling technology to building their own is a recent one as some traditional players like UBS, State Street and John Hancock are still using services from SigFig, Motif or NextCapital. Source.

The Student Borrower Protection Center released a report which digs into how education data in underwriting may be causing educational...

Wells Fargo said their APIs were called more than 1.5 billion times last year as the bank looks to increase...

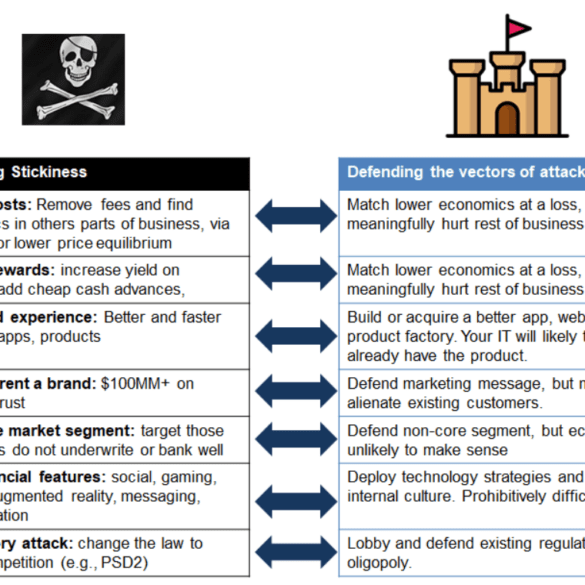

JP Morgan just shut down its neobank competitor Finn, targeted at Millennials in a smartphone app wrapper. Several other traditional banking incumbents have similar efforts, from Wells Fargo's Greenhouse, Citizens Bank's Citizens Access, MUFG's PurePoint and Midwest BankCentre's Rising Bank, as well as most of the Europeans (e.g., RBS competition to Starling called Mettle). These banks have every advantage -- from product infrastructure, to balance sheet, to regulatory licenses, to physical footprint, to relationships with the older generation. So how is it that players like Chime, MoneyLion, Revolut, and N26 are all able to get millions of happy users and the incumbents are failing?