Stash is fresh off a $37mn series D that will see the company double in size and expand into other banking products; the company helps customers invest on behalf of their kids; the typical Stash customer is 29 and makes $50k a year, they help them get more control of their financial lives and invest; “We offer education for these users to help them build the right financial habits from day one, and that doesn’t just stop at investing,” said founder and president Ed Robinson to TearSheet. “Our mission is to help our users throughout their whole financial lives.” Source.

Digital banking startup Stash has been running virtual stock parties during the quarantine as a means of engaging their user...

In this week’s PeerIQ Industry Update they cover the continued crisis across the online lending landscape; even with the crisis...

Fast Company looks forward to 2017 after a rough 2016 for fintechs; highlighted in their five fintechs to watch in 2017 is real estate technology firm Cadre which has closed more than $500 million in inventory; wealth management company Stash also made the top five; the company has gathered over 300,000 users and recently raised $25 million from a Series B funding round; Cross River Bank, a community bank which has close ties to the marketplace lending industry, also made the list; the company provides a banking infrastructure to many fintech firms and recently raised $28 million in new capital. Source

Stash has announced they have raised a $65 million Series E round; with the announcement the company has announced their...

Stash has announced it is rolling out new features for its 3 million users; the app will now allow users...

In this conversation, we talk with Brian Barnes of M1 Finance, about finance “super apps”, the cost-efficiencies of robo-advisors, fractionalized share trading, and tackling the titans of the Wealth Management industry. We also discuss the nuts and bolts of the financial infrastructure making this possible.

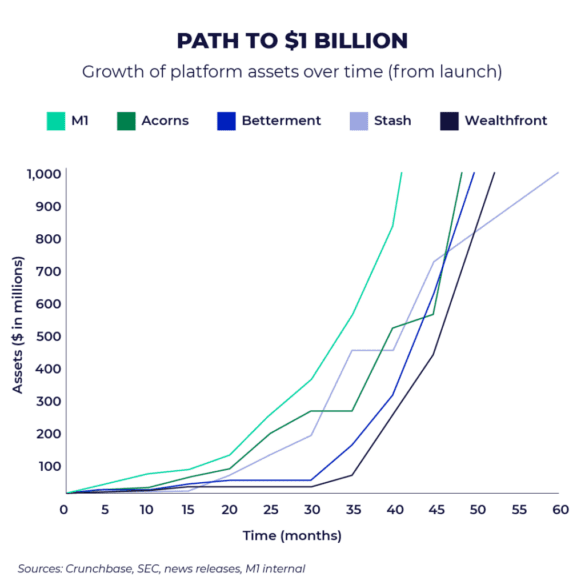

M1 Finance bundles together roboadvisory, neobanking and lending into a single “super app”, allowing for combined pricing power (i.e., charging nothing on asset allocation). The firm currently has $3 billion in AUM, a growth of 50% in the past four months and tripling their total in just over a year. Notably, the company has its own broker/dealer and offers fractional shares, and partners with Lincoln Savings bank on the deposit accounts. That makes for a compelling business model from securities lending, interchange, and order flow.

While some firms are designed to pursue the ultra-wealthy, many are carving a niche in serving the investment needs of the rest of us. Two experts on the topic shared how it's done properly at Fintech Nexus USA 2023 today.

By now most people are familiar with savings apps, many of which help customers save by rounding up purchases or...

According to a survey by Bank of America 77 percent of high net worth millennials own or are interested in...