Put this in the “better late than never” department. Yes, I know it is late July and I am only now just publishing my Q1 2019 returns. Thanks to those of you who reached out but rest assured I am still committed to sharing my results publicly and I apologize for the extreme tardiness of this update.

I am happy to report this quarter that my returns continue to improve. Since hitting bottom in Q2 of 2018 my returns have improved each quarter. Both LendingClub and Prosper showed their best returns in almost two years as the underwriting changes that were implemented in 2017 have had a positive impact.

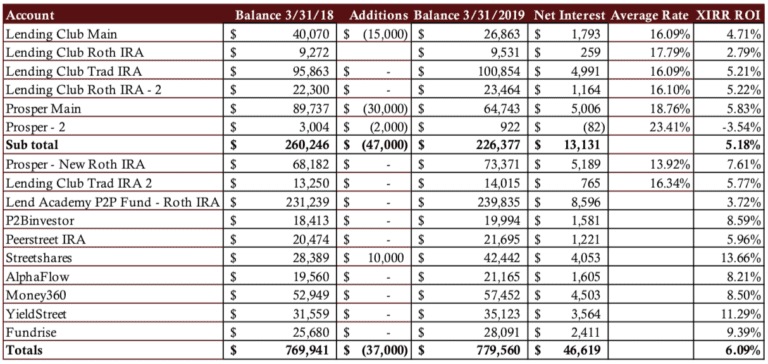

Overall Marketplace Lending Return at 6.09%

My overall returns for the twelve months ending March 31, 2019 was 6.09%. This is up from 5.35% that I reported in Q4 and 4.77% in Q3. My original six LendingClub and Prosper accounts had another full percentage point jump. Last quarter I reported the returns on those six accounts had jumped from 3.19% in Q3 to 4.16% in Q4. We see this quarter they are at 5.18%. This is quite a remarkable turnaround and while I still think 5% is not a high enough return for unsecured consumer lending, it is certainly moving in the right direction.

One point to note is that I am liquidating my taxable accounts at LendingClub and Prosper. I have a little too much exposure to consumer credit in my overall portfolio and so I will be focused only on investing in my IRA accounts there. I am moving my redeemed cash into other marketplace lending accounts as well as other investments outside of fintech.

Now on to the numbers. Click the table below to see it at full size.

As you look at the above table you should take note of the following points:

- All the account totals and interest numbers are taken from my monthly statements that I download each month.

- The Net Interest column is the total interest earned plus late fees and recoveries less charge-offs.

- The Average Rate column shows the weighted average interest rate taken directly from Lending Club or Prosper.

- The XIRR ROI column shows my real world return for the trailing 12 months (TTM). I believe the XIRR method is the best way for individual investors to determine their actual return.

- The six older accounts have been separated out to provide a level of continuity with my earlier updates.

- I do not take into account the impact of taxes.

Now, I will break down each of my investments from the above table grouped by company.

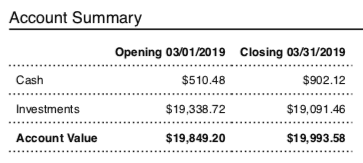

LendingClub

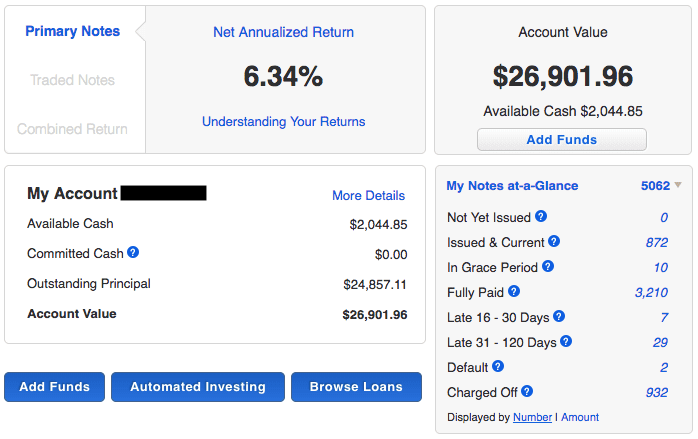

As I said in my last update I am liquidating my original LendingClub account that I opened in 2009 and this will be the last time you will see a screenshot of this account. I am actually a little surprised that even as I have been winding down this account returns are holding up well, at least for now. I stopped reinvesting in September last year, so even with six months of no new notes the returns have continued to improve. Eventually, that will stop being the case and defaults will drag the number down. But all of my LendingClub accounts are improving as the worst looks like it is behind us now.

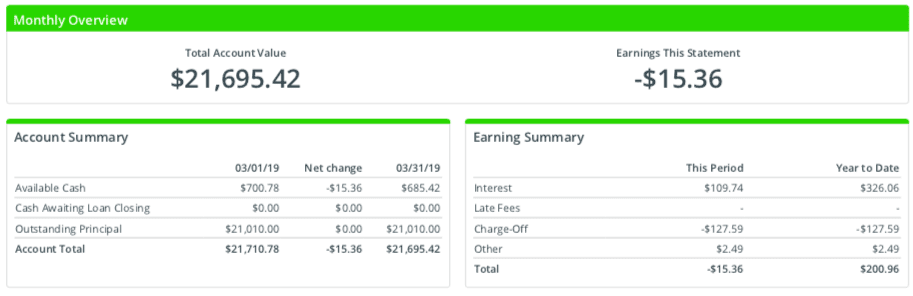

Prosper

Prosper has had an even stronger recovery than LendingClub. I stopped investing in my main Prosper account, which was opened in 2010, back in September as well and the returns are 1.5% higher than Q4 2018. I will continue to reinvest in my IRA account which is my best performing account among Prosper and LendingClub. This was the one account that underperformed for several years because it had a more conservative approach. But that served me well when the higher risk loans started defaulting at much higher rates.

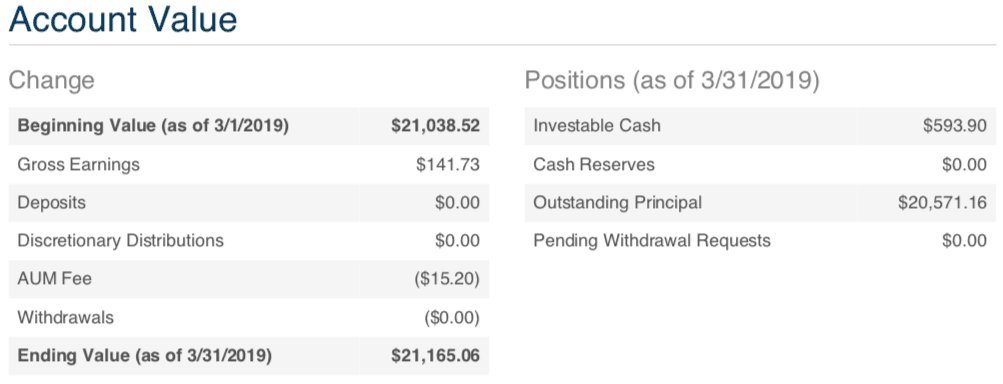

Lend Academy P2P Fund

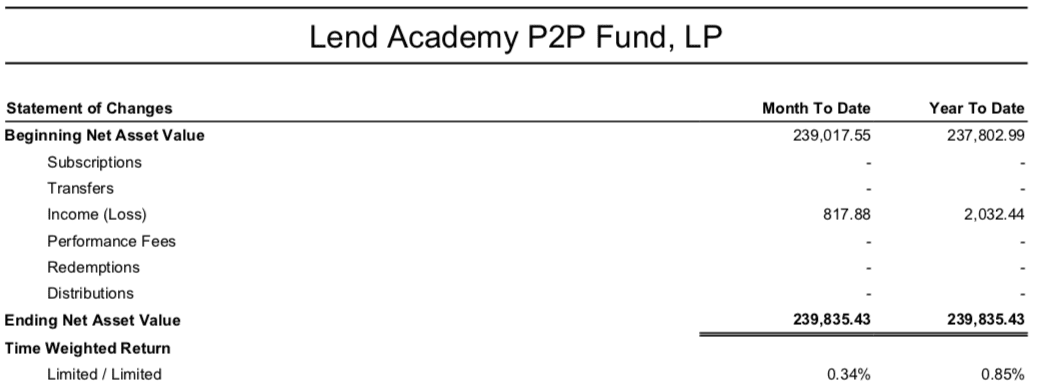

About the only thing good I can say about the Lend Academy P2P Fund, managed by our sister company NSR Invest, is that returns are improving. The TTM return of 3.72% is a full percentage point better than last quarter but we are still underperforming where I would like us to be.

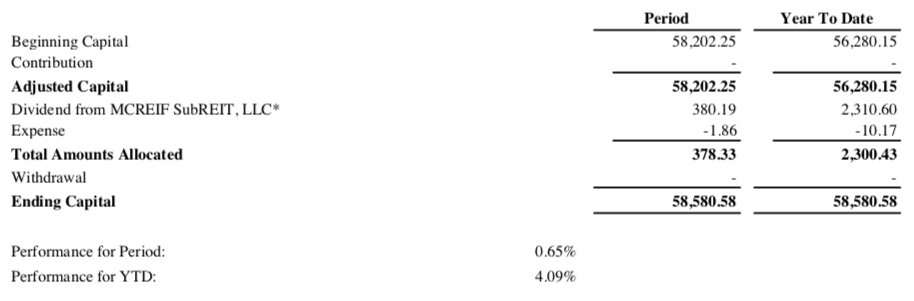

P2Binvestor

P2Binvestor is an asset-backed working capital platform for small businesses that has been around for about four years. Full disclosure, I am on the advisory board of this company and have known the founders since before they began operations. If you go back and look at my historical returns for this holding you will notice that it is a very consistent performer. Every quarter its returns are in the 8-10% range. I have had a little cash drag on this account in recent months as cash builds up quicker than I can deploy it but even with that returns have remained solid.

PeerStreet

I have been investing on the PeerStreet real estate platform since April of 2016. I have invested in dozens of fix and flip properties that have all performed well. But March saw my first principal loss on the platform as a home that PeerStreet foreclosed on was sold at a small loss. I ended up losing $105 (after interest payments) on my investment of $1,000 on this property. This caused my TTM returns to dip under 6% for the first time but I am still happy with the investment and am reinvesting all my principal and interest payments.

Streetshares

Small business lender Streetshares continues to be my best performing account by a considerable margin. I have deposited another $10,000 into Streetshares because of their consistent track record of great returns. Now, it is getting more difficult to deploy capital on this platform and I have received several emails from disgruntled investors who are not able to invest any capital at all. Even when auto-invest is set to invest in every loan often no investments are made for days at a time. I have spoken to the CEO about this and they have said that early investors get preference on these loans. I have been investing since 2015 so I continue to find loans (although I can still go days without deploying any capital) but many new investors find themselves unable to put any money to work. The CEO is encouraging everyone to invest in their Veteran Business Bonds that pay a fixed return of 5%. Clearly that is very different to the returns I am getting but I hope that provides some color on this issue.

AlphaFlow

I opened my account on real estate platform AlphaFlow in August of 2017 when I rolled over an existing Roth IRA account. Then added to this account in Q1 of last year. What I like about AlphaFlow is that they curate real estate investments and then allow investors to easily deploy, even a relatively small amount of capital, across 75-100 properties. I am currently invested in 113 properties across 15 states.

Money360

Money360 is all about bridge financing for commercial real estate. This is not an asset class that is easily accessible for individual investors. The fund invests in bridge loans of $3 million to $25 million across a variety of property types: office, retail, self storage, hospitality, industrial, multi family, manufactured housing and special purpose.

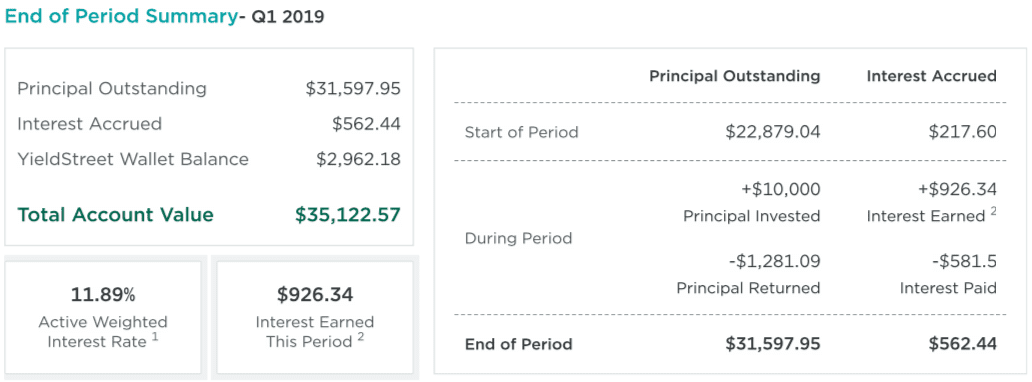

YieldStreet

I love finding esoteric asset classes that are uncorrelated with other kinds of investors. This what you get with YieldStreet. They find interesting investment opportunities that you will not often find on any other platform. I have invested in a portfolio of litigation pre-settlements, a loan for a shipping tanker, and in the second quarter I invested in a loan for vessel deconstruction. The minimums on these investments are quite high, usually $10,000 or more. So, I really like that YieldStreet added an interest bearing wallet last year. While I am waiting for the cash to build up for my next investment I am earning 2.2% on my money.

Fundrise

Fundrise is the only platform that is part of this roundup that is open to to non-accredited investors, beyond LendingClub and Prosper, of course. It is a real estate platform that has created a unique eREIT product that is similar to a publicly tradable REIT but with more transparency and lower fees. I have invested in their Income eREIT which has holdings in 60 projects, mainly multi family homes, apartment building remodels and commercial property. Today, they make investing even easier with Fundrise 2.0 where you can choose from three options: Supplemental Income, Balanced Investing or Long Term Growth.

Final Thoughts

I said in my last update that I need all my accounts above 5% to provide an adequate award for the risk I am taking. While I am not there yet, I like the direction the numbers are heading. And closing down my taxable accounts to focus my investing on IRA accounts will certainly help me come tax time.

Even though I am pulling some money out of my marketplace lending portfolio I am still very much committed to this space. I intend to maintain a balance of around $750,000 for now and will probably increase that to $1 million or more over time. For me, I love the relatively consistent returns that I get from marketplace lending and I expect that if and when the next downturn comes it will perform better than most other asset classes.

Finally, I like to focus on one number at the end of these reports, the total amount of net interest I have earned. As my returns have increased from their lows this number has also increased. My net interest for the 12 months ended March 31, 2019 was $46,619, the highest this number has been in almost two years.