That’s the last straw.

I have to comment on this one and break out of my standard AP-Styled veneer of objectivity for the chance at tipping my two cents into this well.

As an elder Zoomer born in ’97 at the ripe old age of 24, these brands — old and new — are missing the mark. I’m talking about the ‘Crypto Bowl’ commercials, the JP Morgan cafe in the “metaverse” Decentral Land, and Facebook’s Meta stuff coming out this year. It’s all nonsense to me, and I’ve been a digital native since before kindergarten.

Every single headline, some that I have found myself writing, screams of the “how do you do fellow kids” meme. So, if I’m the target audience these giant corpos are breaking their backs and banks to capture, why does it all feel so… desperate?

This chase after web3 and crypto by brands to the point that tradfi said they would start mortgaging barren video game landscapes feels like a combination of the DotCom Bubble, the Beanie Babies frenzy, and the Housing Crash in ’08. I wasn’t even conscious during those calamities, I was six, but it feels like everyone around has forgotten.

Here we go with the opinion

I watched, I guess we’ve all watched as in the past year or two, as the largest tech firms in the world have doubled in value stock-wise. I’m looking at Amazon, Apple, Facebook, Google, Microsoft: they blew up. Traditional finance came right along with them, and the fintech industry I cover exploded onto the public markets while crypto brands burst onto NFL stadiums like expensive billboards.

Now, they are all looking for a new way to add value, give their shareholders a reason to keep buying and send the price up even more. The problem is the reality that you can’t double every year without adding an ecosystem of new, competitive products in entirely new verticals.

Along comes the metaverse, a way to build digital stuff out of nowhere, to sell to those young Zoomers that live online: what a perfect opportunity! At the same time, everyone in the world is stuck inside, with nothing to do but communicate with the internet hive mind! Money printer, start warming up!

With crypto exploding, NFTs flying off the “shelves,” and the comparatively negative costs to build crypto products, it’s no wonder they chose web3. It was either that or branch into extraordinarily competitive zones like housing, space travel, car manufacturing, healthcare, or education.

So while a lot of the rest of us stagnated looking at the stimulus checks that got us nowhere, they started telling us to live boldly and put our money into crypto. It felt like every Superbowl ad was metaverse and crypto-related, and it was terrible.

“Why was it so bad?” You might be asking, “why do million-dollar celebrity deals to promote gambling apps piss you off, Kevin? Is there no fun allowed?”

Well, it stinks because the ads were not made for you, and neither is the metaverse: They’re building it for us, the kids, to capture the next generation before we all forget about dusty old things like Facebook.

This is your brain on Zoomer

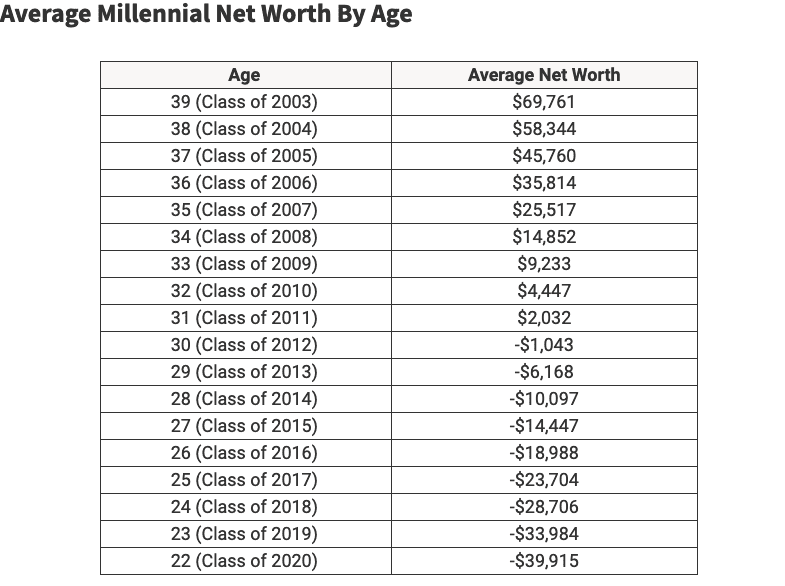

To get in the mind of a Zoomer, what these firms are targeting with their metaverse rhetoric, you have to look below the poverty line. The average young person is in debt, to a tune of $30k in their mid-20s. We don’t have any savings, at all, in the positive up until the age of 33.

Remember, that’s for the older ones; that’s data recorded about millennials that have made it past their prescribed university debt. The jury isn’t even out yet on my generation; remember, I’m one of the oldest, and I have only had a real job post-college for two years.

When anyone talks about Zoomers/Generation Z, ‘the young kids out there dancing on Tik Tok and making weird videos playing video games,’ Remember they are all clueless children in the 10-24 age range. For the most part, Gen Z is not deciders or builders and not a well-established archetype.

The most successful among us are creatives that work within an infrastructure that older generations have built to contain us, like the latticework of social media sites. Blaming us for cringy TikToks and slacktivism is like blaming a hamster for making the most of its cage. Aside from allowances, summer jobs, and entry positions; we’re broke.

When you think Gen Z, remember that most are students under massive debt. Most of us are working hard for teachers who, despite their best efforts, are disconnected from reality, attending schools detached from reality, and consuming a media system infinitely isolated from reality. Remember, higher education students are also the “lucky,” not those working already, through hard work or their parent’s savings grinding through college.

No way to know

For the estimators, the predictors, the Forbes columnists preaching behind grey whiskers: There’s no way to know exactly what we will do. There are assumptions based on nothing, like “oh, they don’t save money,” etc., but I’m the oldest one, and I just learned how to grow a mustache this past year. I’m learning how to save right now because most of you only taught me how to buy, and it’s astounding to me how much we already have on our shoulders.

(And I’m learning through fintech companies, by the way, but that’s a topic for a more positive rant.)

We have yet to see what Gen Z will be, though the leaders are fed up, as you can believe. Why are companies vying for our attention? We are the largest generation block since baby boomers, with 2.5 billion members. According to Bank of America, we will join the workforce in the next decade with over $33 trillion+ in collective earnings.

But we still have some growing up to do.

The oldest of us went through 12 years of relative safety in school that filled our heads with ideas about changing the world. Then, with a cap and gown, or in my case, an email that said: “congrats, get lost,” we were thrown out into the world and realized it was all a scam. It turns out if you’re not getting a Master’s in something that puts ‘Dr.’ before your name, our degrees don’t matter, or our skills are mismatched.

We found out the future is really about finding somewhere to hang out, gathering enough resources to live off of until you die, and that’s it.

For the hyper-connected generation, crypto and hyperactive viral media came along at the right time, a product of millennials who realized the same thing we did: it’s all a big sham, but there has to be a way out. “We are in this together, all across the world, we are all we’ve got, and we can find a new way.”

Crypto adopters are (mostly) gamblers so far

As a kid, the hype and buzz over crypto and metaverse projects is gambling, and the companies running the headlines so far only offer the ability to purchase assets with unknown value. There are entrepreneurs building infrastructure to “onboard the next generation of finance” and there is an incredible demand for it.

My job is to scope out projects and honestly report those trying their best to succeed, not just support anything that mentions crypto. Our own Bo Brustkern went to Eth Denver and loved seeing the excitement over web3 and how crypto combined with trad banking: We’ll be covering it as much as we can.

Unfortunately, besides infrastructure plays right now, enormous piles of money in the industry are selling shovels in a gold rush, and little else. I realized after that statement I just lost thousands of crypto believers, but don’t worry; I may be new, but most crypto supporters haven’t been here that long.

See, I was an early crypto investor. And I know when I say how early you’re all going to say, “no, you’re not.” But in 2017, I first invested in Bitcoin, Ethereum, and a bunch of other crap that went nowhere. I bought in at the height of the hype and the height of the market. Well, almost: I bought Bitcoin when it was around $14,000. I spent 200 bucks of my pizza delivery salary during a winter break from the University of Delaware, studying history, economics, and journalism.

Talk about early adoption: I was hanging out in my parent’s basement in New Jersey, looking at Binance on my phone, and thinking to myself, “Yes, this is the future, this is it. We’re all going to have our own money on our phones; there’s no more work, there’s only play. We’re going to run the world and change everything! We’ll take down every institution!”

Then it crashed

Then, Bitcoin crashed to $3K, and I lost nothing because I put in 200 bucks. As the price dropped, I moved my coins around, investing in altcoins that don’t even really exist anymore, like TRON and BNTL. The guys at Stellar and Ripple still owe me a Lambo, and I’ve been waiting for almost six years: Welcome to the bag-holding party. Even if I kept it in Bitcoin, today it would be worth $550? What a revolution!

So I didn’t lose everything, but I lost the spirit that many of you still have, that crypto is the way out of here. Today, that idea is the metaverse and web3, but it is the same sentiment. It turns out no one remembers 2018: most people bought in during the bull run in the last two years, and most devs started in this field since then. Sure there were times to make x1000 gambles since I lost my spirit, but you see how we are talking about investing in unregistered securities now, not database technology?

What I’m saying is, I’m a gambler too. Just stop calling it “democratizing” when I pull the handle of the slot machine.

The oldest people in crypto are either fortunate, basement-dwelling devs, buyers of angel dust on the Silk Road in 2013, or even worse. There are few real OGs that knew it was big before the price explosion brought in the rest of us. The remainder is the truest grifters the world has ever seen.

That’s the real problem. It’s all utterly dumb luck, and anyone that got lucky a decade ago currently owns a mining company, and the recently fortunate own a crypto punk or bored ape profile pic and post like they know what they are doing.

Blockchain, smlockchain

The concept of blockchain, a public indisputable database ledger propped up on a somewhat decentralized validator system, is neat. The numbers, the cryptocurrency that can run on that database might hold promise. It may be the future or maybe a piece of the puzzle. But if I’m honest, I don’t think digital gold will change everything, and even if it does, I don’t think we are all getting taken along for the ride.

The old version of money, before fiat, was paying someone to dig money out of the ground. The intermediary was paying for a share of government trust.

This new version, paying for graphics cards to turn electricity into coins, isn’t that innovative.

“But Kevin, That’s POW, POS is the future!”

OK, so should the people with the most share control the system? Again, that’s supposed to be revolutionary?

Crypto ain’t crypto, bitcoin ain’t bitcoin

Most crypto we interact with is centralized, offered through a service like Coinbase, and liquidity layers like Tether, and far from the ideals that predicted it would change the world, but closer to the purpose of lining the pockets of the early adopters. Don’t get me wrong; I love Coinbase; I was in Times Square beside their team for the IPO and have been a user from the beginning.

Still, they are just a company trying to profit on a trend using new tech and run into massive adoption issues.

Turns out, while crypto fans can make up complex sounding words that mean “bean counter,” I can clap back with “human nature.”

Do you think the most prominent institutions on the planet — the banks, the government, the people that print money, even tech giants like Facebook — are going to let you build a system where they’re not involved, where they’re not in control? I mean, are you kidding me?

On the opposite side: do you think that the people who are building the tools of the new world that say, “we’re offering a new decentralized way to trade, a new, wholesome way to sell virtual ownership unlike anything before!” Do you think those people have your best interests at heart? Do you think they’re just more intelligent than everyone else, different from the last band of techies that built web2, that crypto engineers are just not human?

Human fallibility

Unfortunately, just like web2, the new wave of startup devs are human, and they suffer from all the same problems, like greed, fear, malice, and self-interest. But, most importantly, they care about making money, and who can blame them? They are us.

So when the new rising tech barons say the old tech barons are evil, that their new tech will be better than the old, am I missing how it’s new?

Even looking at bitcoin itself, it is a collection of devs that implement new ideas onto a relatively ancient blockchain code: it’s still centralized to a small team and virtually unscaleable. It transacts seven times a minute and uses more than half as much electricity as Italy or the UK.

Anyone on earth can recommend changes. At any time, the primary users of the chain, the centralized oligopoly of liquidity providers like Coinbase, Binance, or worse yet, whoever prints Tethers, can choose a new fork to validate, and everyone in the world has to listen. It has happened before.

Decentralized? What about when a government blocks addresses for crowdfunding border blocking? Uncorrelated? What happens when war in the east is feared, and crypto drops like a rock to mirror the S&P?

Obsessed with blocks

That’s how crypto feels to anyone who isn’t completely obsessed. You could spend time on crypto Twitter and be convinced otherwise by a bunch of people spouting words they just learned, but you’re either selling it or you’re losing money.

Full disclosure, I’m not a no-coiner. I’m in Solana, Bitcoin, Link, Eth, Cake, doge bonk, Cardano, and others, and I still feel this way. I have an OpenSea account; I’m looking forward to Coinbase’s new NFT “Insta.” I’ve even minted NFTs hoping that someday someone will choose my PFP line of generated smiley faces to launder money.

Despite my high horse, I wish I had put 1,000 bucks on Shibu a year ago, so I could retire and laugh at the world from a throne made out of gold. But, don’t get me wrong, it’s not like retail investing in stocks is any different, I wrote a whole research paper about Robinhood’s PFOF, and little has changed since Bernie Madoff invented the thing.

The problem is that maybe three people get lucky and early on things like Shib and convince followers to be loud about it, and soon enough, everything is an echo chamber, and everyone sounds like they are getting rich. Meanwhile, the signs of a bear market have been here for two months, and it’s like no one remembers how crypto went cold like the grave after the last crash in 2018.

Winter is coming to borrow an ancient meme.

MORE METAVERSE FUD: NFT wash trades are common

Digital internet pogs have captured attention spans everywhere. With hideous, generated sneers, they illustrate problems with crypto adoption.

NFTs. Celebrities buy them, and sports stars sell them, but sports memorabilia has always been a cash cow. To the attuned crypto investor™, the NFT craze looks precisely like the altcoin mayhem in 2018. Back then, having a “team” and a “whitepaper” was enough to inspire millions in crowdfunding from speculators, who dodged rug-pulls like digital landmines.

The problem with the hype is it’s easy to whip up from nothing, and in crypto, it’s easy to hide behind semi-anonymity. Some statistics show that the billions of dollars in the top 100 transactions on NFT websites are trades between a couple of accounts.

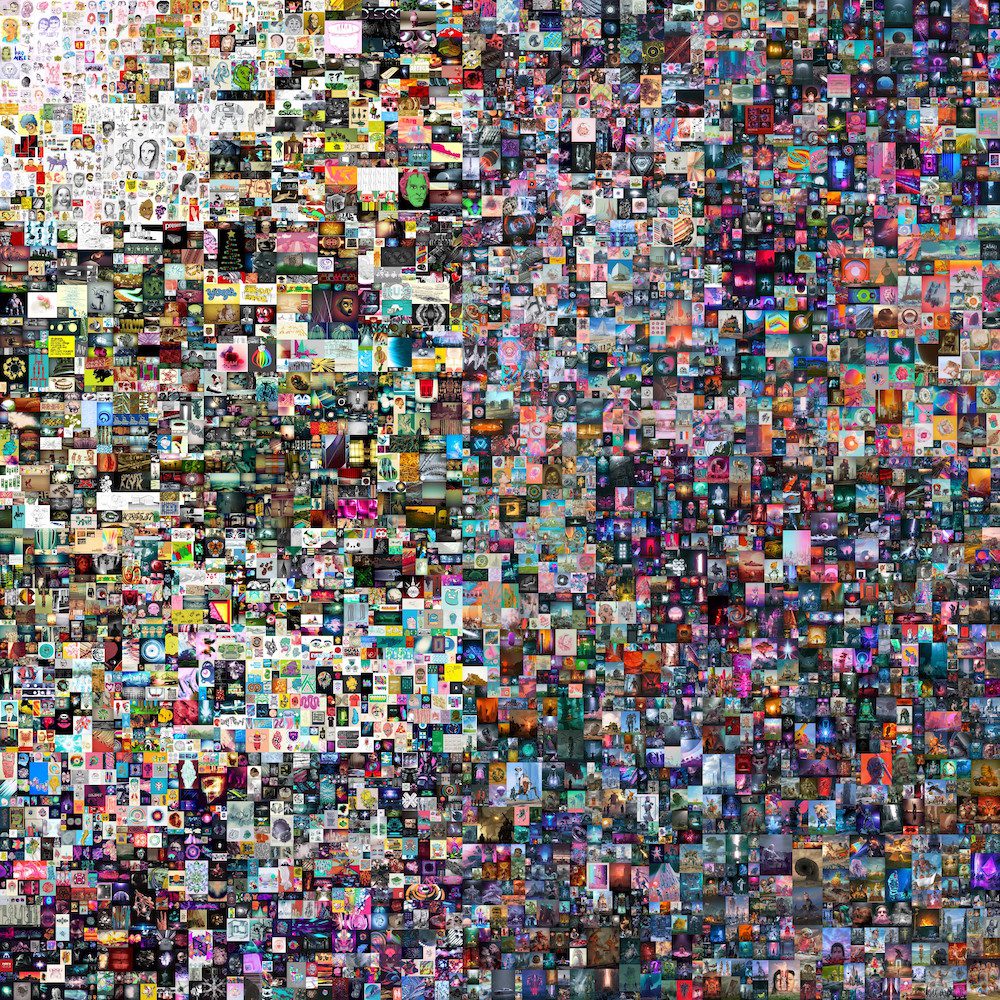

Take the historic sale of Beeple’s Everydays project that started this whole NFT run last year. He sold thousands of absurdly childish drawings through Christie’s, all collected into one big pic. Remember that?

What a year it’s been.

Anyway, it fetched more than $60 million, but there was a catch: Beeple’s alleged confidant bought it. Before the auction, the artist made friends with an art investing group called Metapurser, which had purchased a collection of his work only months before. The group had set their sights on a new crowdfunded purchase of plots of land to show the Everydays project and built a Beeble coin called B 2.0 to do it; and Beeple got 2%.

“It was important for us that the artist was taken care of beyond the sale proceeds, so Beeple gets an allocation of 2%,” the group wrote on Medium.

Price skyrocketed

As the day of the auction came and went, the coin price skyrocketed more than X1000 from $.30 to $20, since returning from orbit at about $.50, if anyone is interested in buying. That would net Beeple about $3 million, and more for the creators who held over 50% of the coin if they sold.

So a guy he already knew picked up the tab, and they wash traded the “artwork.” Now, they’re building a Metaverse 3D area where you can look at the art.

So much for crypto, the actual sale is unsearchable on the blockchain and may as well have been in cash. In my opinion, they scammed the whole world by pretending they bought something and launched NFTs into the mainstream. It was a bidding war with no one, and I bet you didn’t even know.

As the New York Stock Exchange eyes added NFT trading, Reuters reported the common occurrence of a handful of NFT accounts swapping ownership hundreds of times, giving the illusion of volume.

Unfortunately, that’s how a lot a whole lot of stuff works in the crypto world, and not just recently. People have been inflating digital coins since Satoshi first blog-posted.

To ignore that fact is to be sucked up in the premise that new technology can save us from all ills when in fact, we’ve always been people, and new tech shows us who we are.

What do the Zoomies want then, bud?

When I look at my friends, and I think, what do we want out of new tech and new products, I don’t see people getting ready to go online and put on a VR headset and pretend we’re in a video game and we’re waiting in line at a virtual bank.

When I see JP Morgan’s pdf about metaverse money, their weird lobby in Decentral Land, and the awful-looking tiger someone bought with real-world money at that company, I don’t see that as anything like the future.

I’ve been playing Minecraft since before it was released, since I was 12, and I love that game. I go back to it every couple of years; It’s really fun. But, do I want to live there? No. In my spare time, I want to spend time with my friends.

Sure, I’ll have one or two nights a week where I like to hide by myself, listen to music, watch YouTube, or a movie, listen to podcasts, play video games in my little world: That’s true, and maybe that’s unique to my generation.

Urge to be ‘in person’

But when Friday ends, I want to go to a bar and spend time eating food, seeing live music, drinking, and playing cards, in person. As soon as I finish writing this article, I’m going home to my apartment to spend time with my roommates.

Covid came along and interrupted that and made us all go online, and now it’s like major businesses think it’s never going to end: that we all WANT to sit inside all day.

Instead, it just taught me the magic of spending time in person with my loved ones, and I bet all of you feel the same way. Hybrid work modes are new, and zoom is here forever, but do any of us WANT to go in VR to our work when we can sit in our PJs in a home office?

It’s hard to tell where the metaverse, crypto, and all of it is going, but like all new tech: most of it is complete BS. Made-up marketing from PR people with nothing to do, for bored news writers like me, to type up. At its best, the metaverse already exists in the video game world. People have been trading in-game currency and rare skins for decades, and adding blockchain doesn’t change anything.

At its worst, it’s them trying to find a way to get us to pay for more stuff because their stocks doubled in price last year, and they have nothing to show for it, and investors like me want the money number to go up again.

In the end, when Facebook launches its product, it will be better, but still. I would rather see Fortnight or Roblox, or Minecraft build a Metaverse hangout zone than Facebook.

I refuse to call them Meta, by the way. Their lack of new ideas since 2008, converting a dating app into a news publisher, crashed the tech market a couple of weeks ago. Besides developing the astounding Ocrolus Rift VR Headset, I don’t think FB knows how difficult it is to build video games.

That’s really what all of this is, by the way. The metaverse is video games, except they want us to live there.

Give me a better app

When I look at my paycheck on my phone, at Fidelity or Chase Bank or PNC or Venmo, I don’t want to choose my shirt and shoes. When I’m pricing out a hotel room for my time off or predicting how much the weekend will break the bank, I don’t want to walk to the bank digitally: I want an app that works better.

I genuinely believe that my phone will be in my brain one day soon, and I’ll be able to close my eyes and connect to everything in the world. I guarantee it. Besides my complaining, I’m looking forward to it; carrying around a piece of glass filled with electricity as my stem into the human experience is annoying.

It will be under our skin and updated through cell division, and even then, it’s going to be depressing, annoying, and flawed. But there won’t be virtual corporate waiting rooms and lines for bank tellers: that’s nonsense.

We live the Metaverse

Gen Z is a group of people already forced into believing and sucking into this horrible money pit, an anxiety-depression-filled zone of abuse and consumption. At least in America, at least in my demographic, my peers are depressed people.

A third of women I know are fighting eating disorders because of what they are shown on Instagram. Meanwhile, every guy is chronically lonely, looking for connection and community, buying whatever they see in social ads targeting grief and manliness. We didn’t need a whistleblower to tell us that it was by design: we already know. We live it.

No one with money to spend gives a damn about any of that, and those taking part in all virtual sales like NFT flipping or video game skins are speculators. Children who spend their parent’s money; 10-year-olds who don’t know the value of goods are into that stuff right now.

Maybe I was, too when I was 12, buying skins for video games like Team Fortress 2 or Runescape.

But as you grow up, you start to care less about experiences like that. As I matured, I started enjoying building my computer more than playing games anymore. And that’s what I think all these metaverse metaphors talk comes down to; games.

Internet as a third place

The ‘metaverse’ is just the internet as a third place, the devs that run the current world reaching further into our everyday lives, highlighted by the recent scarcity of physical third places.

Like all inventors, they’re taking advantage of a trend, trying to get us to believe in something new, to see their vision of what the world could be. That vision may come from benevolence, but it’s only human.

In contrast, I don’t think my age group wants anything more than to spend time with their friends in person, feeling the brunt of an uncaring, howling, angry planet that’s currently running on the web 2 operating system.

Devs run our lives already, with app designs that would ensnare even the smartest hominid. Generation Z already lives in the metaverse: you are too if you’re reading this article on a screen. All this new stuff is marketing.

I don’t think any of us Zoomies are looking forward to whatever web3 will force us into doing; we are already exhausted with the need to be digital all the time.

It’s necessary, vital, and essential for commerce, but I don’t think it’s any of our choices.

So when I see JPMorgan has a weird lobby to set up lending in some unheard of HTML-based Sims copy, I think of Second Life and Club Penguin, coolmathgames.com, and other things I did online when I was five.

I don’t think of the future of finance, and I believe no one should.

{kind=link}