[Update: an earlier version of this post had the preliminary return number of 6.20% as I awaited for the final statement. I underestimated the closing balance there so my actual return was 6.30%]

Time for an update on my quarterly investment returns. This is something I have been doing for many years now and I know it is appreciated by many of you. I started out reporting on my marketplace lending investments in Q4 2011 and have provided updates every quarter since then. I share all the details of my LendingClub and Prosper investments as well several other investments I have made in the online lending space.

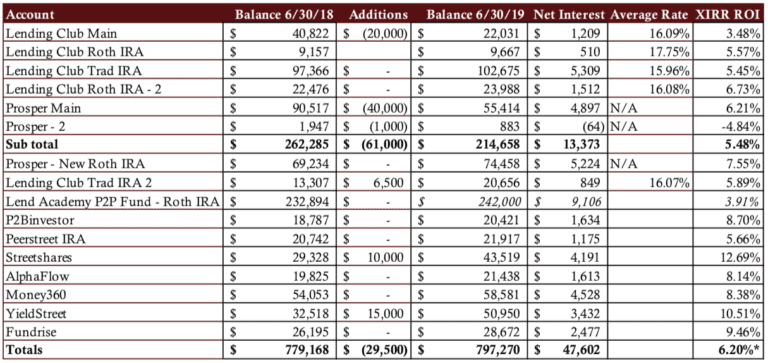

Overall Marketplace Lending Return at 6.30%

The upward trend in my returns continued in Q2, making it the fifth quarter in a row with increasing returns. My preliminary return for the 12 months ending June 30, 2019 is 6.30%, the best I have achieved since Q3 2017.

My six original accounts at LendingClub and Prosper have all been open for at least seven years so they are very mature accounts that have experienced several turns of capital as I have kept reinvesting over the years. I have separated these out because these were the accounts I had when I first started doing these reports so readers can go back and see how they have trended over time. But as I have said before I am liquidating my taxable accounts here and will focus my investments in consumers loans in my retirement accounts.

Underwriting changes that were made in 2017 continue to bear fruit for my personal loan investments. My six original accounts had a return of 5.48%, a vast improvement from the 2.34% return of just a year ago, and back to near where it should be. In today’s benign credit environment I would still like to see returns in the 6-7% range for personal loans and we are headed in that direction.

Now on to the numbers. Click the table below to see it at full size.

As you look at the above table you should take note of the following points:

- All the account totals and interest numbers are taken from my monthly statements that I download each month.

- The Net Interest column is the total interest earned plus late fees and recoveries less charge-offs.

- The Average Rate column shows the weighted average interest rate taken directly from LendingClub. Prosper no longer shows this information.

- The XIRR ROI column shows my real world return for the trailing 12 months (TTM). I believe the XIRR method is the best way for individual investors to determine their actual return.

- The six older accounts have been separated out to provide a level of continuity with my earlier updates.

- I do not take into account the impact of taxes.

- My Lend Academy P2P Fund returns are not final which is why there is an asterisk in the ROI numbers.

Now, I will break down each of my investments from the above table grouped by company.

Lending Club

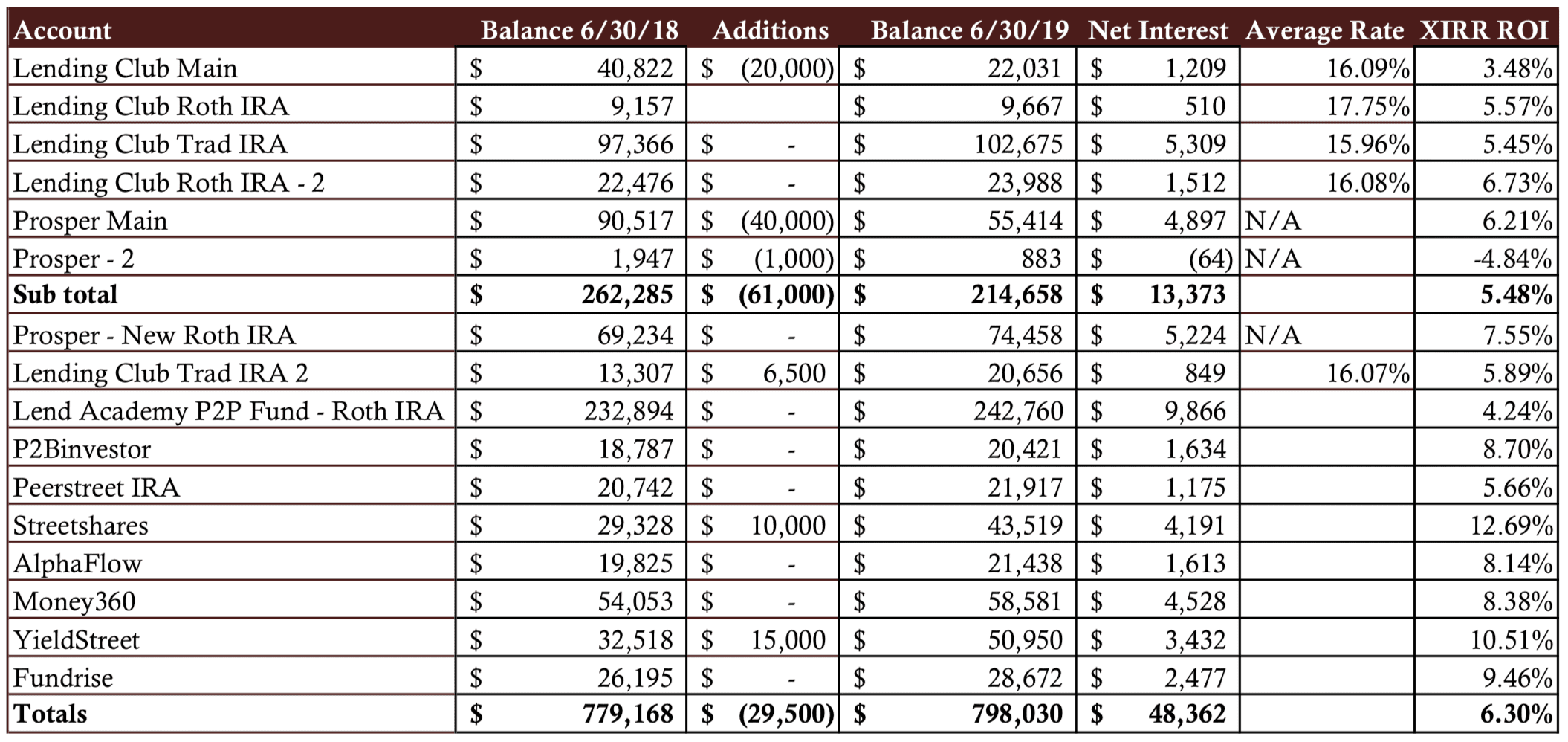

Above is a screenshot of what I call Lending Club Traditional IRA. This account was opened in 2010 where we rolled over a 401(k) my wife had in a previous job. It was just over $53,000 that we initially deposited and we have reinvested all principle and interest since that time. So, the account has almost doubled in value since 2010 and that initial investment has resulted in over $500,000 in principal plus interest payments as that money has been cycled several times into new loans. I have been very pleased to see the improvement in returns at LendingClub over the past year. While I have been winding down my taxable account, given this improvement I was comfortable putting in a new $6,500 into the traditional IRA account held in my name.

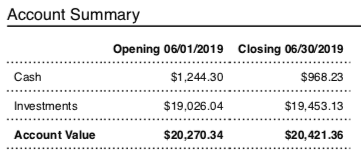

Prosper

My Prosper accounts have also been doing really well compared to a year ago. Apart from the tiny account I have been winding down both my taxable and IRA accounts have been performing well. The above screenshot is for my Roth IRA account that was opened in 2014 with a $50,000 investment. This account is managed by NSR Invest using their balanced approach which has been my most conservative account over the past five years and it is no coincidence that its performance has held up well. My taxable account here is being wound down as I put my focus into non-taxable accounts for Prosper and LendingClub.

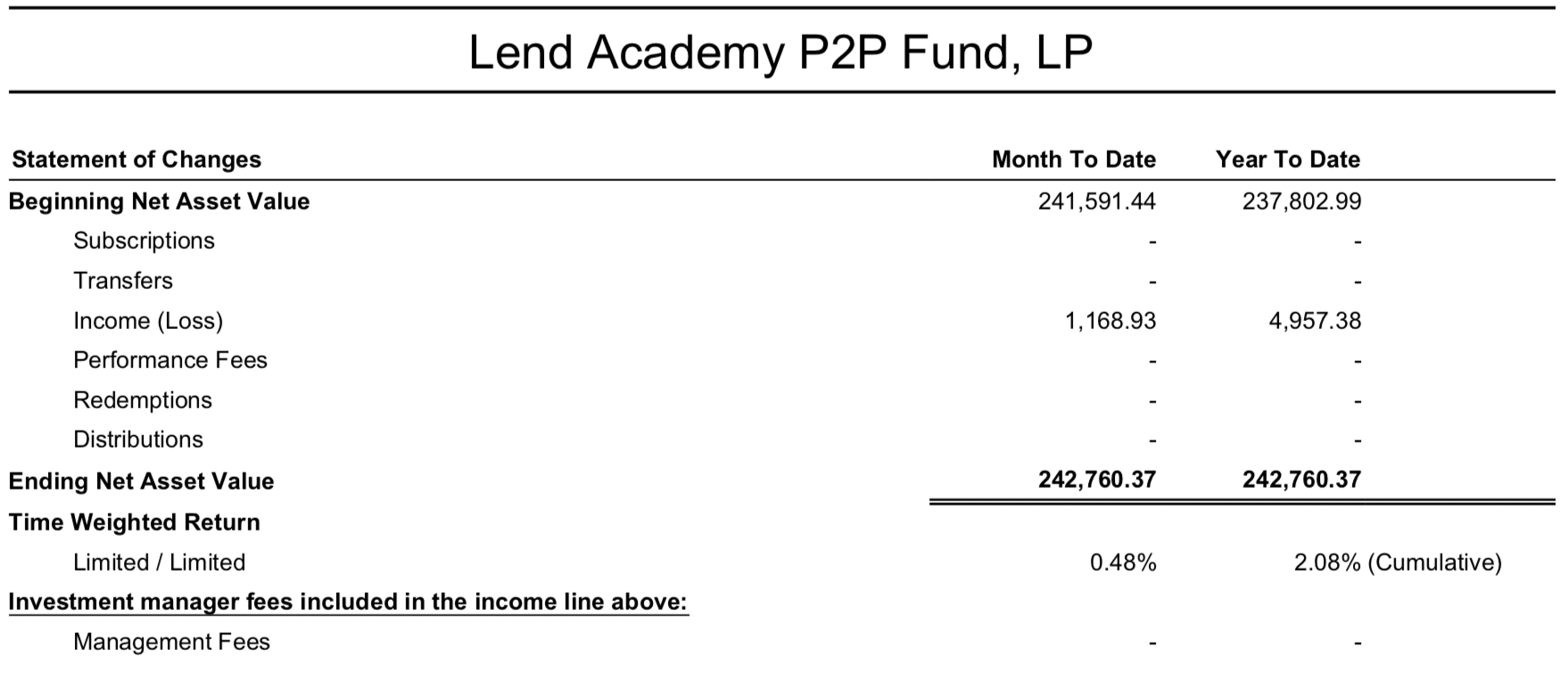

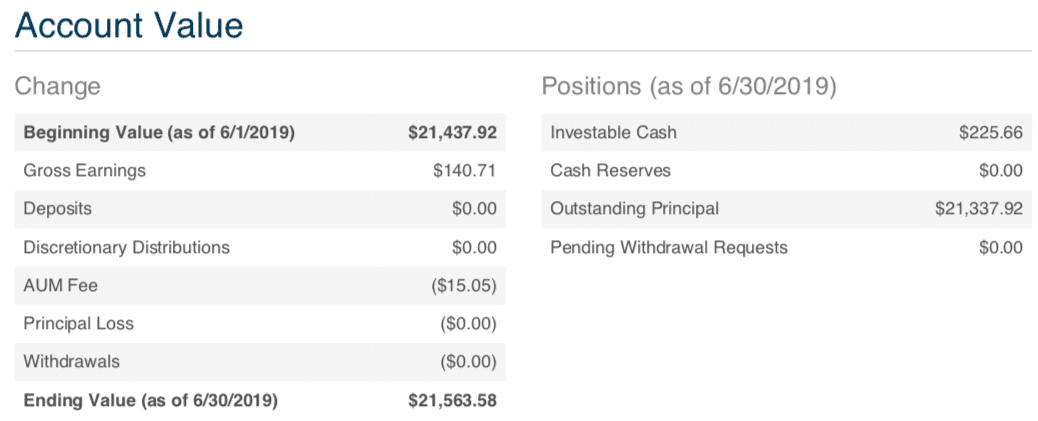

Lend Academy P2P Fund

[Update: Q2 statement displayed above]

We are still awaiting final numbers for The Lend Academy P2P fund for the the second quarter. I have included our estimate which should be close to the final number. I will update this section when that is final.

P2Binvestor

P2Binvestor is an asset-backed working capital platform for small businesses that has been around for about five years. Full disclosure, I am on the advisory board of this company and have known the founders since before they began operations. P2Bi continues to provide consistent returns in the 8-10% range. I am investing in lines of credit typically backed by accounts receivable so unlike most of the investments here these are short term loans with 30-60 day liquidity.

PeerStreet

I opened my PeerStreet account about three years ago when I decided to put money to work at the real estate platforms. The expected returns are as high or higher than consumer credit these days and your investment is backed by a hard asset. PeerStreet focuses on short term loans – typically 6-24 months with yield to investors in the mid to high single digits. I like the $1,000 minimum per investment at PeerStreet which has enabled me to feel comfortable starting with a relatively small investment. I have cycled through my initial capital several times already as the payback on many of these loans ends up being less than 6 months.

Streetshares

Small business lender StreetShares continues to be my best performing investment as it is still showing a solid double digit return and has done so for many years. I have added to this investment over time but I will probably stick with what I have as it is getting more difficult to deploy new capital. I invest in every single loan they make available and even then I still have maintained a considerable cash balance which has been a drag on returns. I heard a rumor that they are closed to new platform investors now as they are pushing everyone into their Veteran Business Bonds that pay 5%.

AlphaFlow

I opened my account in real estate platform AlphaFlow in August of 2017 when I rolled over an existing Roth IRA account. What I really like about AlphaFlow is that you can quickly build a diversified portfolio of 75-100 properties as they deploy new money across multiple lending platforms. Also, since I am not an expert in real estate investing I appreciate the fact that they provide expertise in selecting the very best properties from these different platforms.

Money360

What I like about the Money360 fund is that it gives me access to large commercial real estate loans. This fund, called M360 CRE Income Fund LP, provides exposure to short term bridge loans for commercial property with loans ranging in size from $3 million to $25 million. These are 12-month to 36-month loans with an LTV of less than 75% and broad geographic diversification.

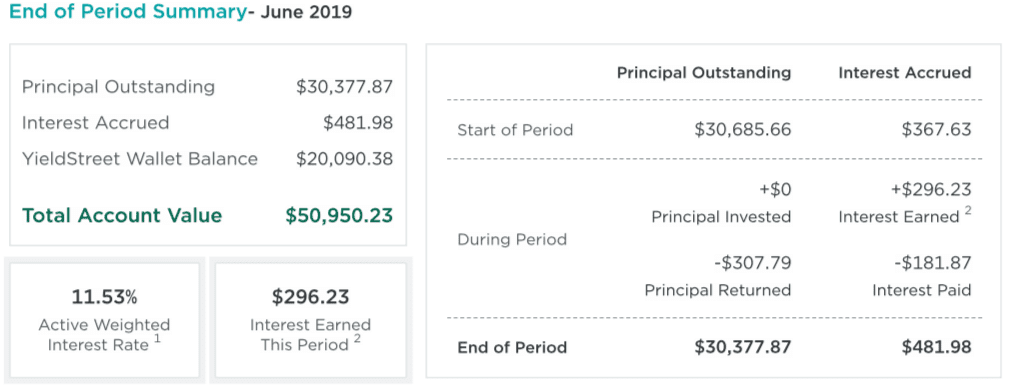

YieldStreet

YieldStreet is the most unusual platform in my portfolio. They look for unique asset-backed investment products such as real estate loans, secured business loans, litigation finance and marine finance. I have invested in a litigation finance offering consisting of a portfolio of plaintiff advances related to 365 different personal injury cases. I have also invested in a credit facility collateralized by up to three tanker vessels, a very unique offering. These two offerings are both paying north of 10%. They also pay good interest (1.7% as of this writing) while your cash is parked so I didn’t mind keeping over $20,000 there as I wait to deploy my capital into the next deal.

Fundrise

Fundrise is a real estate platform focused on the individual non-accredited investor. I opened up my account there more than three years ago and I continue to be impressed with their consistent returns. I am invested in their Income eREIT fund which is currently invested in 66 projects, primarily multi-family home construction. New investors can get started with just $500 and build a diversified property portfolio with their simple investment plans.

Final Thoughts

I have been very pleased by the comeback in the consumer loan segment. I have also learned my lesson. For many years I chased the highest risk loans and while that produced fantastic returns for quite some time it ended up being a bad decision as I was left with barely positive returns for a year or two. Now, I am invested across the risk spectrum and seeing better and more consistent results. I will not be able to achieve double digit returns again here but I am ok with that. With a recession likely in the not too distant future I want to stay well diversified, erring on the conservative side, when it comes to risk.

While I still like the personal loan asset class I have been trimming my positions here and investing into other asset classes as you can see in this report. Many of these provide consistent returns that are uncorrelated with most of the other investments in my portfolio.

Finally, I like to focus on one number, the total amount of net interest I have earned. Like my overall returns this number continues to rebound with my net interest for the 12 months ended June 30, 2019 over $47,000.

* Estimate based on an estimated conservative return for the Lend Academy P2P Fund. Final number will be updated before next quarter’s report.