As Banking-as-a-Service develops into Embedded Finance, who holds the responsibility of compliance gets decidedly murky.

This week, we look at:

Over $1 billion in raises announced last week, and over $10 billion in Fintech company value creation: Checkout.com with $450 million at a $15 billion valuation, Affirm more than doubling after its IPO to $30 billion, lending enabler Blend raising $300 million, and payments enabler Rapyd raising $300 million.

A systems theory framework that explains the stocks and flows of goods and services, and what monetization strategies are available to fintechs

How transactional models are thriving and creating 50-100x revenue multiples

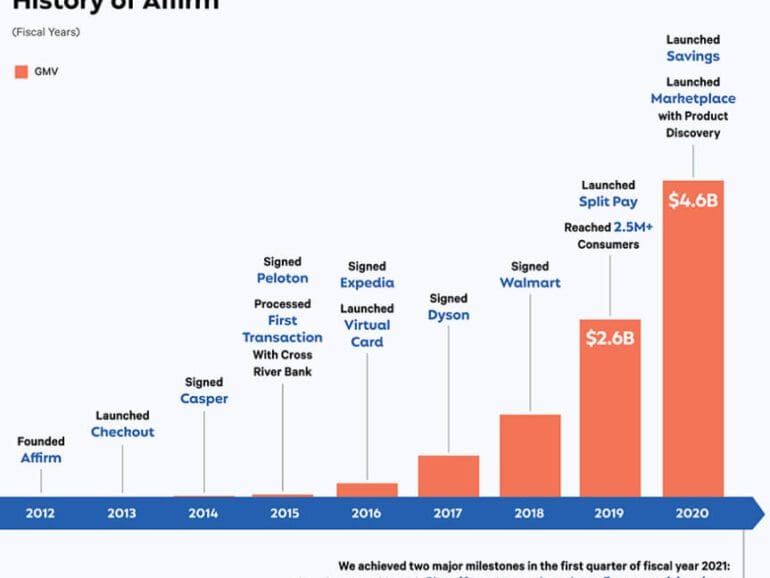

I have been reading Alibaba: The House that Jack Ma Built this week, something everyone interested in understanding the future of Google, Goldman, Uber, or Amazon should do. The narrative starts with China's small business explosion, and Ma's genius is to tap into global demand for the products of those businesses through an online marketplace and associated financial services. But I am getting ahead of myself. Let's pause to acknowledge a massive, systemic transaction that was announced this week: payments processing company Global Payments acquiring TSYS (Total Payments Systems) for $21.5 billion.

This week, we look at:

Embedded finance as a growing theme with the $10B Affirm IPO and Stripe's launch of Treasury

The customer types that each of these firms is attempting to convert into their product, and what this tells us about economic growth

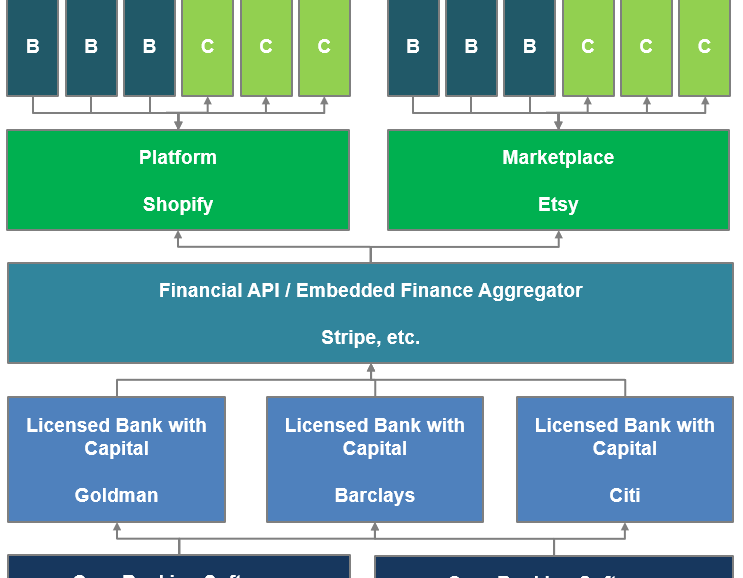

A framework for understanding the emerging value chain of digital finance, and the role of platforms and marketplaces

This week, we get philosophical and look at:

Embedded finance and how it will be woven into the fabric of the Internet

Applying the philosophies of existentialism, nihilism, and absurdism to Finance

Parsing symptoms in decentralized finance (Based Protocol) as artistic protest

Finding Dadaist beauty in chaos

In this video conversation we feature a roundtable by The Defiant exploring how and if the gap between Fintech and DeFi will be bridged.

DeFi Panelists

Lex Sokolin, head economist at ConsenSys

Santiago Roel Santos, angel investor

Spencer Noon, Investor at Variant

Vance Spencer, co founder at Framework Ventures

Fintech Panelists

Keith Grose, head of Plaid international

Nik Milanovi?, founder of This Week in Fintech

Simon Taylor, co-founder of 11:FS

Bruno Werneck, Business & Corporate Development at Plaid

Moderator

Camila Russo, Founder of The Defiant