[Editor’s note: Many people have been discussing Lending Club’s somewhat lofty valuation so I thought it would be useful to bring in a valuation expert to do some analysis. Ho Wan Lee, CFA, CAIA, is a senior associate in the valuation group of Arcstone Partners LLC. Arcstone specializes in the valuation of high-growth companies and complex securities. Current and former clients include some of Silicon Valley’s best known tech companies.

Note that neither Lending Club nor Prosper are clients of Arcstone, nor does Arcstone have privileged information relating to Lending Club, which is the subject of Lee’s analysis below. The analysis is the unique work of the author and is based entirely on information available to the public. Mr. Lee’s analysis is provided for informational purposes only, does not constitute an opinion of value, and should not be construed as investment advice.]

Lending Club (“LC”), the world’s largest online marketplace connecting borrowers and investors through its online lending platform, is expected to launch its IPO in the coming weeks. The amount of the raise and the IPO placement price are still unknown at this point in time, but according to an article in the Financial Times the Company is anticipated to raise more than $500 million with an implied valuation of about $5.0 billion. One question apparently on everyone’s mind is this: is a $5.0 billion valuation reasonable?

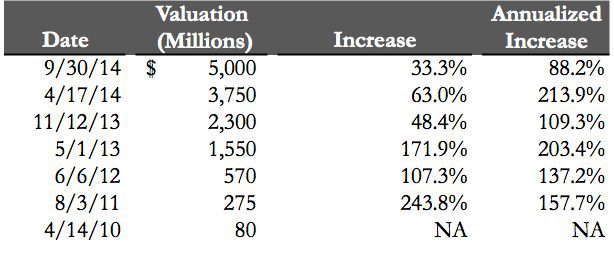

The Company has shown rapid appreciation in value over the last several years. It was valued at $3.8 billion in April when it acquired Springstone, a company that facilitates education and patient financing. So to begin, a $5.0 billion IPO valuation represents a 33.3% increase in value from April of this year, and an annualized increase of 88.2%. Certainly, some of this increase in value could be explained by what we valuation analysts refer to as a “liquidity premium”, which essentially reflects the increase in value when a stock is freely tradable. Moreover, comparing the implied increase to the historical increase in observed valuations of LC while still a private company, the jump in price does not seem outrageous.

Table 1: LC’s valuation over time

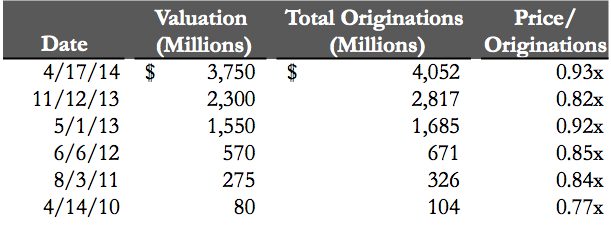

So that’s one way to look at the $5.0 billion implied valuation. What about valuation multiples? Looking at LC’s venture round pricings on a multiple of total originations, it has remained relatively consistent in the 0.8x – 0.9x range. If we assume a 0.8x origination multiple, a $5.0 billion IPO valuation would imply LC’s total origination of $6.3 billion as of September 2014, which is not unreasonable considering LC’s recent trend.

Table 2: LC’s Valuation/Originations over time

(Origination numbers source: nickelsteamroller.com)

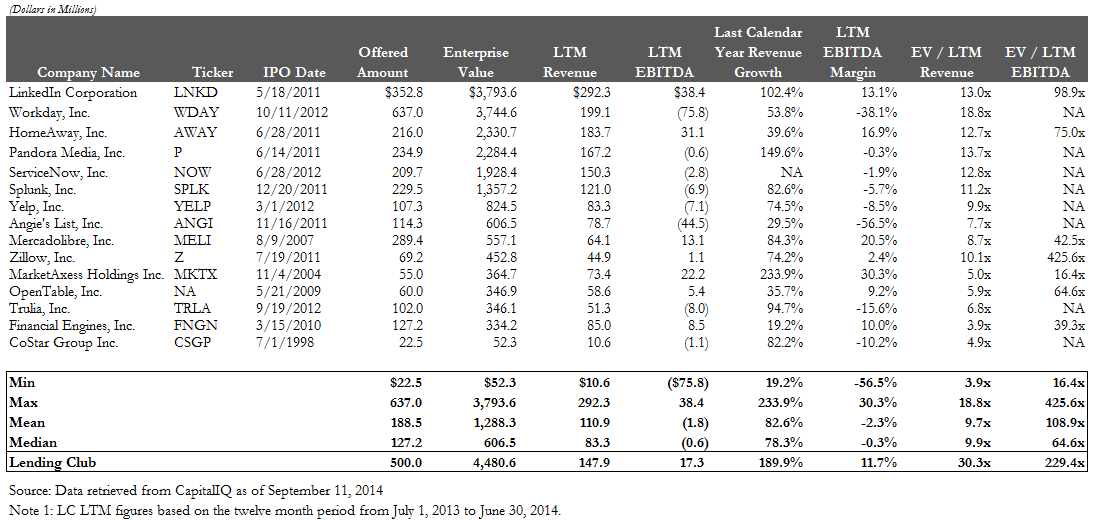

Now what about multiples compared to comps? Based on the Company’s revenue for the 12 months ending June 30, 2014, the $5.0 billion valuation implies an enterprise value (“EV”) to trailing revenue multiple of approximately 30x. In LC’s S-1 filings, company management identified a list of public technology companies as their compensation peer group, which they selected based on consideration of revenue, revenue growth, net income and market cap. It is important to note that these companies are not necessarily valuation comps as they were identified as compensation comps in the S-1. However, the peer group does provide insight regarding management’s expectations about the Company and provides a potential benchmark for LC’s IPO valuation multiples. To assess the implications of the estimated $5.0 billion valuation for LC, we consider LC’s implied revenue multiple of 30x relative to trading multiples of comps as well as their IPO multiples.

Table 3: LC’s executive peer group’s operating metrics and valuation multiples

(click on the image below to view at full size)

Table 4: LC’s executive peer group’s operating metrics and valuation multiples at IPO

(click on the image below to view at full size)

As seen in Table 3, the implied revenue multiple of 30x for LC far exceeds the current trading multiples of comps, with only Workday coming close. Similarly, as seen in Table 4, LC’s implied revenue multiple of 30x is also substantially higher than the IPO multiples realized by the comps. From 2012 to 2013, LC experienced net revenue growth of 189.9%, which places it at the high end of the comps (the only company that had last calendar year growth at IPO higher than LC was MarketAxess Holdings, which experienced 233.9%).

One other notable metric to consider is revenue scale. Typically, revenue growth tapers as scale increases since it becomes harder to achieve further penetration as a company increases market share. Notably, for the twelve-month period ending June 30, 2014, LC has already reached a revenue scale of $147.9 million, which puts it at the higher end of the comp set at IPO for revenue scale; yet the Company was able to generate higher growth than all but one of the comps. Indeed, over the last several years, the Company was able to achieve substantial growth in revenue through consistently growing loan originations, as well as improving profitability. We note, however, that LC’s profitability actually declined in the year-to-date period ending June 30, 2014 primarily due to increase in compensation expenses.

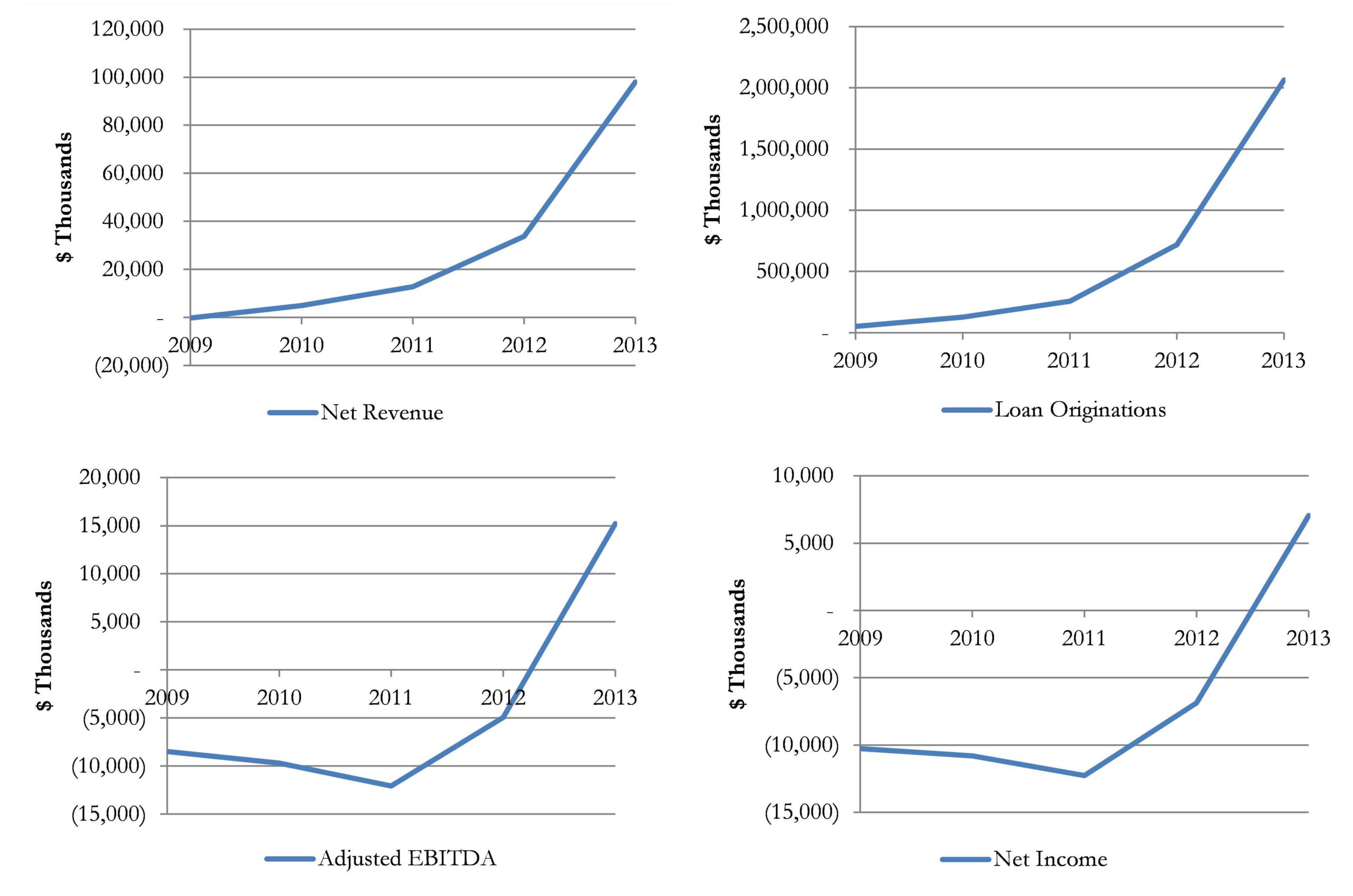

Charts: LC’s operating performance pre-IPO

Data in the charts below were retrieved from LC’s SEC filings

Although LC was able to generate high revenue growth to date, in order to justify the high valuation, investors need to believe the Company will be able to continue attaining extraordinary growth (keeping a similar growth trajectory as in the past few years) and leverage its operating efficiency to achieve high profitability in the future. Essentially, the high valuation assumes LC will be able to achieve its mission of transforming the banking system.

Based on LC’s S-1 filings, the Company believes further expansion is achievable through:

- Enhancing the product suite. The Company expanded into the small business loan market in March 2014, and has also branched out to education and patient loans with the acquisition of Springstone.

- Widening the spectrum of borrowers served. The Company plans to extend the product offering to wider risk profiles to meet demand.

- Entering into strategic partnerships with banks, asset managers, and insurance companies.

- Continuing to invest in its technology platform and data sources to connect an increasing number of borrowers and investors, identify new borrowers, detect fraud and maintain the security of the platform.

- Exploring international opportunities. The Company currently operates in the US, but intends to expand the platform to address similar banking system inefficiencies, market dislocations, investor needs and borrower dissatisfaction globally.

However, we believe the following are significant risk factors that could affect the Company’s success. This list is not meant to be exhaustive and additional risk factors exist, some of which are presented in the Company’s S-1 filing:

- The Company may not be able to continue growing its loan originations and revenue in the future.

- The Company may be unable to maintain relationships with issuing banks.

- Increased competition may negatively affect future earnings potential.

- The Company may be negatively affected by regulatory and compliance mandates.

- Fluctuations in interest rates could negatively affect transaction volume.

- Failure to maintain information security of the platform can negatively impact confidence in the business.

- The Company had positive earnings in 2013, but incurred net losses in the six months ending June 30, 2014 primarily due to an increase in compensation expenses. Fluctuations in earning may continue to occur, and the Company may not be able to achieve profitability going forward.

So what’s the answer? What’s it worth? It ultimately depends on your assessment of the Company’s prospects for growth and profitability, as well as your perceived risk of the investment. To justify the estimated IPO valuation, it is clear that LC needs to continue achieving astonishing growth, which is however not impossible given its unique position in a huge industry and its impressive track record. How will the Street receive the Company? It will ultimately be priced according to the different valuations that market participants place on the Company’s stock. My guess is no better than yours.

I wish you good luck as you embark on your own analysis of this interesting company.