In 2018 QuickFi set out to bring innovative tech to equipment finance, a $1 trillion industry in the U.S. stuck in the stone ages. Today, QuickFi gives instant, completely digital access to capital for 29 million small businesses and growing.

Founder and CEO Bill Verhelle said that QuickFi was founded to provide speed and 24/7 self-service financing deals itself. Still, the firm aims to license out its premier tech so that equipment dealers can offer financing right on the lot with just a few clicks, and a banking partner can fund deals easily.

“People don’t realize how big equipment finance is: $2 trillion worth of equipment is sold every year in the U.S., and half of that, or 1 trillion, is financed,” Verhelle said. “The problem that we saw: getting that financing, especially in small increments to creditworthy business borrowers, is costly … there was so much friction in getting those small amount loans to creditworthy borrowers.”

In 2020, things changed; everyone realized the importance of digital solutions, even in the equipment financing world, Verhelle said.

Since that tipping point, his firm has won a slew of awards, like the Banking Tech Awards best use of I.T. for Lending, the 21′ winner for Innovative Commercial Finance Platform, USA, from the Pan Finance Innovation Awards, and a nominee for LendIt’s Emerging Lending Platform.

Timing is everything

A lot of problem solvers in the fintech space say, “How do I get underbanked people financed or people who don’t have credit,” Verhelle said. “We said, look, there’s a trillion dollars a year worth of people already financing stuff, and it’s painful.”

Banks and other funders offering loans weren’t happy either, only getting a small amount of interest income on some of the loans, while the borrowers paid a high rate. There had to be a change.

Verhelle and the team built QuickFi coming from a lifetime of experience in the equipment finance space, he said. He first founded First American Equipment Finance 15 years earlier, implementing new tech like CRM and video calling to make life easier. Verhelle departed in 2015, three years after City National Bank bought FAEF in L.A.

“We grew that business over a long period of time, and today First American is Royal Bank of Canada’s U.S. equipment, finance business. It’s still called First American, which is ironic since it’s owned by a Canadian company now.”

‘I was out, but they pulled me back in’

For the next two years, Verhelle was no longer with the firm, and he was waiting for his non-compete to end. He fell back into the equipment finance world when former colleagues approached him about building something new.

“Mark Tomaselli, our President; our Chief Credit Officer Mike Ziegelmann; Courtney Dioguardi, our SVP; and COO Nate Gibbons … those folks all wanted to leave First American to do something new,” Verhelle said.

They all joined the new venture, but not for any bad reason; Verhelle said the new buyers were great, but the team wanted to build something new.

They settled in on what they knew best, with the freshest tech they could design, Verhelle said,

“Mark, our president, and the person with the most technology background pushed, saying ‘let’s not do a ‘me too’ business, let’s do something revolutionary, let’s do something bold and different that, 10 years from now, everybody’s going to say, you know, they did something that mattered — they made a difference.'”

The platform

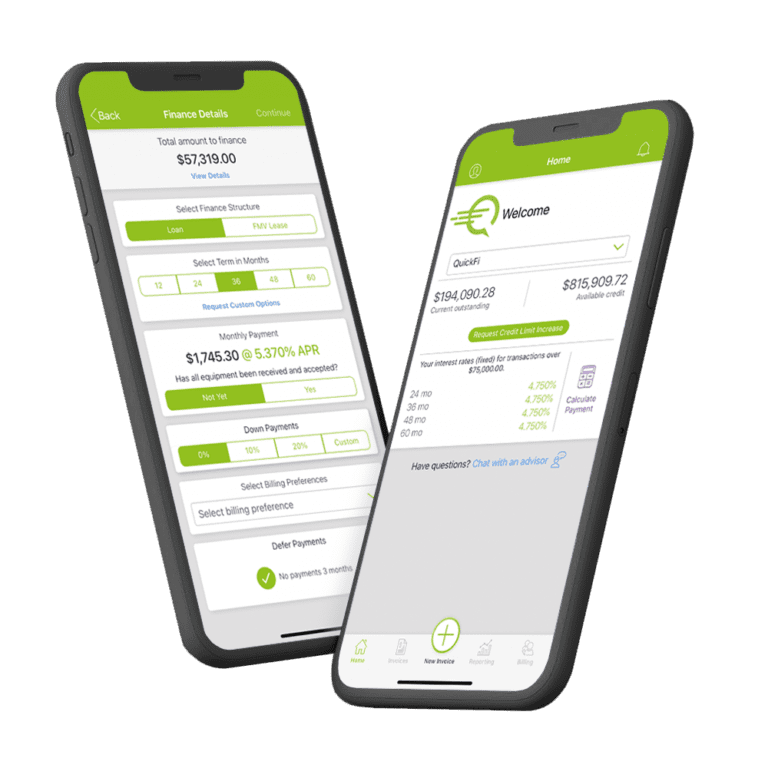

The team created a one-stop-shop for financing, from account creation, business credit scoring, KYC authentication, driver’s license check, and even facial recognition and blockchain — all in three to four minutes, Verhelle said.

“That’s a one-time process; after that’s finished, there’s a three-step process to finance new equipment. And that can be completed in another three minutes,” Verhelle said. “Once a customer has an account with a line of credit, they can use it repeatedly; all the servicing and support is available through the app; it’s available 24/7.”

Instead of the traditional method of calling up a finance company, waiting for a proposal, going back and forth negotiating, singing, waiting for credit approval, QuickFi takes an iota of the time, Verhelle said.

A customer can go through and be approved in the middle of the night, and the funds land the next business day.

Verhelle called out the SMB loan world, which tends to lack disclosure of metrics like APR due to the type of agreements SMB owners make with most funders.

“But small businesses are often taken advantage of because of that, so we disclose the APR on every single loan, even though it’s not required by law in the U.S. We also have no fees, no hidden costs,” he said. “So it’s a very transparent, very borrower-friendly financing.”

A lot of the users come from partnerships between QuickFi and global equipment manufacturers and their dealers, who can refer customers to the QuickFi self-service app for financing right on the lot; Verhelle said, “They can complete the purchase and financing right there on a Saturday morning standing in a muddy parking lot … financing the excavator and putting it on the trailer before driving it away.

Looking for partners that understand the trade

As Verhelle explained, their business model originally included holding the loans on their balance sheet and funding the loan in-house. However, once they perfected the platform, they realized that white labeling and encouraging banking and funding partners to fund the loans was a better play.

“We’d much rather bring a bank partner or somebody with a balance sheet to take the loans. Then we can focus all of our attention on perfecting the platform and adding new features and technology, and continuing to build the platform.”

He said they have a trial system set up, so a partner can test out funding deals where QuickFi underwrites the credits, takes all the risk, “they can stand it up and run it for a couple of months, see how it works for their dealers, and see how it works for their customers. And it takes us like a week to get that set up and rolled out. They can try it almost instantly.”

Verhelle also described his product as an output of digital contracts that are not held on the QuickFi balance sheet for long. Instead, those digital contracts can be used by the manufacturer to raise funds, shifted to banks for safekeeping, or held by a partner to securitize or used to build a line of credit with their banking partner.

Repeat customers

Joseph Vu, Digital Marketing Manager at QuickFi, pointed out that while the team had channeled energy to creating a product that gave the first-time customers a seamless experience, as almost a byproduct, they had produced a perfect setup for repeat customers.

“Most people, when they enter the business, and they’re working on transactions, and they focus on the singular transaction: they want to get it across the finish line,” Vu said. “This was just a secondary consequence of what we’ve built: repeat transactions. So there’s value to both our partners and value to us, in that we’re able to help a business transact over the lifecycle of what their business would need.”

The ease of use helps dealers give better service to customers who have expected mobile applications for some time now, Vu said. Although SMB owners are used to digital banking for their consumer accounts, they say it’s excellent it finally carried over to a business function.

The hardest part of innovating in a traditional space

Verhelle said it’s hard to do something brand new.

“I just think back about the time you spent in your career in business, and most of our experience in business is essentially working as an optimizer,” Verhelle said. “When I think about my career — and we did some innovative things, and we’ve some great successes in a prior business – but much of the time you’re not creating anything new, you are just optimizing … you’re turning a dial on the machine, checking the output, trying to adjust very minor business optimizations.”

When doing something completely new, there is no playbook to follow, no guide to check, Verhelle said.

It’s why, in a trillion-dollar business, the most prominent trad players aren’t trying to change a thing, even if the end consumer, and American business owner, are worse off.

But, now that economies of scale have kicked in, Verhelle said the results are amazing. According to industry data from the Equipment Leasing and Finance Association in Washington, DC, QuickFi comes in at a fraction of the cost.

“Industry survey data includes high volume participants like Wells Fargo, Caterpillar, John Deere, but even operating at scale, the cost is high for small-ticket equipment finance transactions: about $2,900 per transaction with the old system that everyone uses,” Verhelle said.

If you’re going to start a new equipment finance company, you need to buy millions of dollars of software and hire up all these different people; and you’ve got to run it for years to get it to scale.

“We charge our partners less than a third of that amount for our 100% digital platform. So it’s both better, and it’s less than a third of the cost. And as we get to scale, we think we can take it to a 10th the current cost,” Verhelle said.

“It’s instant, it’s digital, it’s got all these advantages, but it’s also so much less expensive to operate. And rarely do you ever get a business opportunity that is both cheaper and better.”